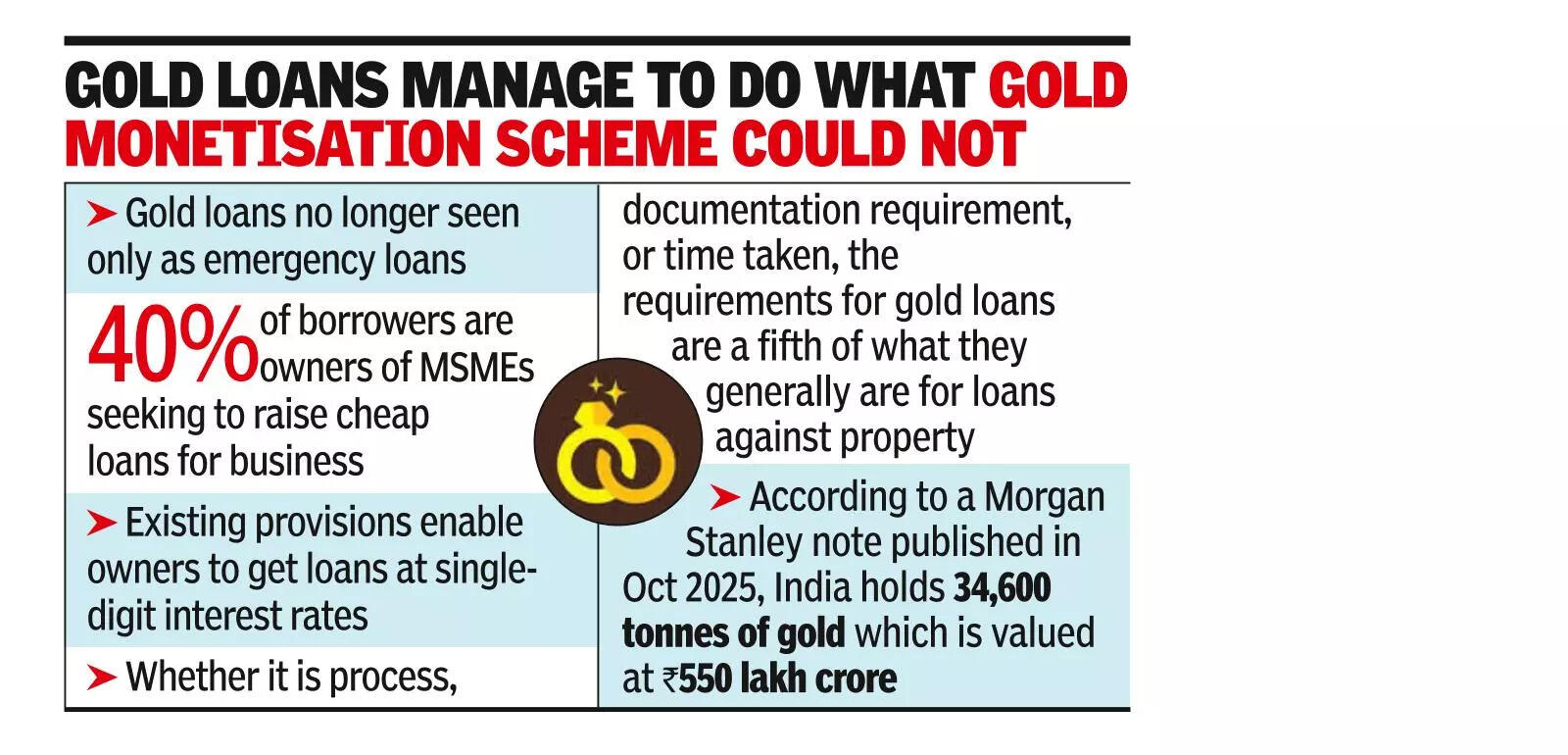

MUMBAI: Behind the triple-digit growth numbers in gold loans is a structural change in the way Indians are viewing their family jewellery. Hocking ornaments of the women of the house, which was earlier seen as a sign of distress borrowing, is now being viewed as a way to monetise ancestral jewellery and bring down the cost of financing a business.Historically, gold loans were dominated by borrowings below Rs 2.5 lakh, as these borrowers accounted for 60% of gold loans. According to credit bureau CRIF, in FY25 their share dipped to 51%, and for the first eight months of this fiscal only 40% of loans are for below Rs 2.5 lakh.In 2015, RBI attempted to bring out the gold idling in household lockers through a gold monetisation scheme that would provide interest on gold deposited with banks. The catch was that ancestral jewellery would need to be melted into bullion, tested for purity, and then deposited with banks. However, owners saw the melting of jewels as the destruction of artistic value, and the scheme did not succeed. “Gold loans have managed to do what the gold monetisation scheme could not. While the craze of wearing jewellery has gone down, the desire to own gold has not. Gold loans enable owners to get loans at single-digit interest rates,” said Shripad Jadhav, head of Bharat Banking at Kotak Bank.According to Jadhav, gold loans are set to overtake loans against property to become the second-biggest loan category after home loans. “Whether it is process, documentation requirement, or time taken, the requirements for gold loans are a fifth of what they are for loans against property,” said Jadhav. He added that gold loans are no longer emergency loans and that 40% of borrowers are owners of MSMEs seeking to raise cheap loans for business.According to a Morgan Stanley note in Oct 2025, India holds about 34,600 tonnes of gold, which has a market value of approximately Rs 550 lakh crore. As against this, the value of gold loans in India stands at around Rs 15 lakh crore, against which Rs 25 lakh crore worth of gold is pledged.“Benign credit costs are another driver of profitability for gold-loan NBFCs. Losses have been historically low because of the collateralised nature of these loans, high liquidity of the underlying precious metal, and well-established auction processes. Credit costs have stayed below 1% over the past five fiscals and are expected to remain low,” said Prashant Mane, director, Crisil Ratings, in a recent note.

Why gold loans offer win-win proposition