Motilal Oswal maintained its “buy” rating on Eternal with a price target of ₹380, which implies an upside potential of 34% for the stock from current levels. The target of ₹380 is higher than the current all-time high on the stock, which is ₹368.

The brokerage in its note analysed Eternal’s three businesses — the recovering food delivery business, the quick commerce business, which continues to scale despite intensifying competition and the nascent going-out business District.

According to Motilal Oswal, Eternal’s food delivery business is stable with an improving trajectory and Blinkit remains a generational opportunity in hyperlocal commerce despite near-term growth normalization. It expects profit after margin of 2.5% and 3% for the company in FY27 and FY28, respectively.

Motilal Oswal said Eternal has guided for $1 billion in adjusted EBITDA for the consolidated business by FY29. The brokerage estimates $500 million for quick commerce, $425 million for food delivery and the balance being contributed by the going out/District/Hyperpure business.

Food delivery business

Motilal Oswal said the food delivery business’s net order value (NOV) grew 16% in the financial year 2026, with growth accelerating for the third consecutive quarter after bottoming out three quarters before.

The recovery has been driven by deliberate product interventions, such as lower minimum order values for Gold members and a sharper focus on value-conscious consumers, it said. Platform fee increases also continue to support revenue per order, while profitability remains within the management’s guided range.

For the first quarter, Motilal Oswal expects the business’s NOV growth of 19.7% from the previous year, with a 21.5% take rate and adjusted EBITDA margin of 6.1%.

Motilal Oswal continues to view the food delivery business as a stable duopoly and model 20% NOV growth over FY27-28, with margins gradually moving toward the guided 5%-6% range.

Quick commerce

The brokerage said District continues to scale despite stifling competition.

It said the competitive intensity remains high across the category as players compete through pricing, lower minimum order values and promotional offers.

Despite this, Blinkit has crossed adjusted EBITDA breakeven and mature markets are already generating 5-6% EBITDA margins, it said.

Its store count stood at 2,243 by the end of the March quarter, with the management on track to reach 3,000 stores by March next year.

The brokerage said Blinkit’s growth is moderating from exceptionally high levels, but the management’s guidance of over 60% compound annual growth rate (CAGR) over the next few years suggest the demand remains strong and the category remains underpenetrated, even in mature markets.

While Motilal Oswal estimates quick commerce growth to moderate at 70% this fiscal, it sees this as normalization with improving unit economics and a clearer path to profitability. It has factored in gradual margin expansion, led by store maturity and operating leverage.

For the first quarter, Motilal Oswal expects Blinkit’s NOV to grow 84.4% from last year, with contribution margin at 5.2% and adjusted EBITDA margin at 0.6%.

District

The brokerage said District remains in its early stages. However, the concert economy is becoming more meaningful. India’s live events market is already ₹20,000 crore to ₹22,000 crore with an annual growth pf 18% – 20% annually. Ticketing is contributing to 50% to 60% of overall topline.

The demand is also improving, with 70% of the urban GenZs, millennials attending at least one live event annually and marquee events continuing to witness 85% – 90% fill rates despite higher ticket prices, Motilal Oswal said.

As Eternal expands beyond food and quick commerce into the wallet share of the affluent urban consumer, the brokerage believes District presents meaningful optionality and could contribute $125 million to its EBITDA by FY30.

Of the 34 analysts who have coverage on Eternal, 31 have a “buy” rating and three have a “sell” rating.

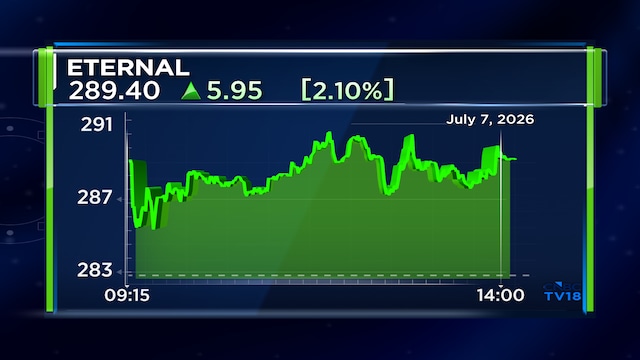

Shares of Eternal are trading 2.2% higher on Tuesday at ₹289.65. The stock is up 17% in the last one month and has hence turned positive on a year-to-date basis.

Also Read: Trent shares fall 12% after Q1 update – Five things you should know