For steel companies, average steel realisations are expected to rise by around ₹4,000 per tonne quarter-on-quarter, driven by price hikes implemented over the last two quarters. However, the benefit is likely to be partly offset by higher input costs, particularly elevated coking coal prices and higher iron ore costs.

Steel companies are expected to report around 8% year-on-year volume growth, although volumes may decline by about 14% sequentially due to seasonal factors. Capacity ramp-ups at Jindal Steel and JSW Steel are expected to support overall shipment growth.

Sector margins are likely to improve by around ₹1,500 per tonne in Q1 FY27, supported by stronger flat Hindalco Industries. However, the gains could be moderated by higher coking coal costs and seasonal weakness in rebar prices. While hot rolled coil (HRC) prices have remained relatively stable, rebar prices have come under pressure and are expected to remain weak during the monsoon season.

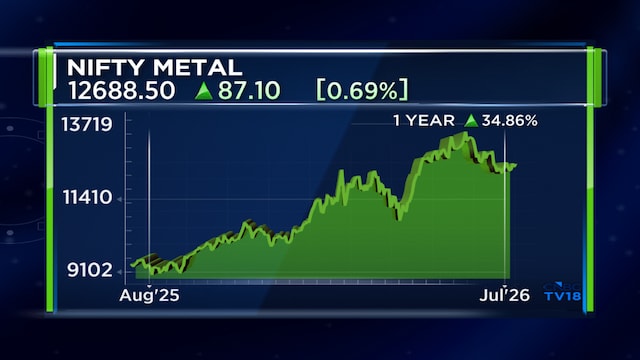

The outlook for non-ferrous companies remains broadly positive, supported by strong commodity prices. During the quarter, aluminium prices rose around 12% sequentially, while zinc prices gained about 7%. However, silver prices declined over the same period.

Watch the full conversation here

According to Jefferies’ estimates, Hindustan Zinc is expected to post the strongest sequential earnings before interest, taxes, depreciation and amortisation (EBITDA) growth of around 14%, followed by JSW Steel at 11%. Coal India is expected to report a marginal decline, while Tata Steel could see EBITDA fall by around 4%. Shyam Metalics and Energy is expected to report a 7% decline, followed by Jindal Stainless at 11%, while NALCO may post the sharpest sequential EBITDA decline of around 13%.

On the stock-specific front, Amit Murarka, Executive Director of Axis Capital expects Hindalco and NALCO to be among the strongest performers this quarter, supported by higher aluminium prices and strong physical market premiums.

Going forward, however, he prefers ferrous stocks over non-ferrous names, citing the potential recovery in rebar prices after the monsoon. He sees JSPL and JSW Steel as key beneficiaries of the improving demand outlook, while also remaining positive on Coal India due to stronger e-auction volumes, better pricing and potential value unlocking through subsidiary IPOs.

Catch all the latest updates from the stock market here