The brokerage expects the sector to see capital expenditure over the next five years, as companies build a competitive and integrated solar manufacturing ecosystem in India.

This, it believes, will act as a key entry barrier and a differentiator among players.

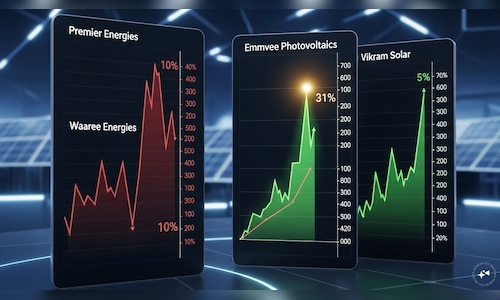

Waaree Energies

JM Financial has initiated coverage on Waaree Energies with a ‘Reduce’ rating and a price target of ₹2,815 per share, implying a downside of 10% from current levels.

The brokerage expects steady growth driven by capacity expansion and strong order visibility, with revenue, EBITDA, and profit after tax projected to grow at compound annual growth rates of 34%, 42%, and 40%, respectively, over financial years 2026 to 2028.

However, it believes current valuations already factor in these positives, while aggressive diversification and capital deployment limit near-term upside.

Premier Energies

Premier Energies has also been initiated with a ‘Reduce’ rating and a price target of ₹816, implying a 10% downside.

The brokerage expects the company to sustain strong growth, supported by capacity additions and deeper backward integration. EBITDA margins are likely to peak at 29% in FY26, aided by operating leverage.

While JM Financial values the company at 10 times FY28 estimated EV/EBITDA, it believes current valuations cap near-term re-rating potential.

Emmvee Photovoltaics

The company has been initiated with a ‘Buy’ rating and a price target of ₹291, indicating a potential upside of 31%. The positive stance is driven by its strong integration capabilities and scope for valuation re-rating as scale improves.

The brokerage expects cell and module capacities to rise to 4.7 gigawatts and 7.9 gigawatts, respectively, by FY28, translating into revenue, EBITDA, and profit after tax growth at CAGRs of 83%, 77%, and 87% over FY25 to FY28.

Vikram Solar

Vikram Solar has been initiated with an ‘Add’ rating and a price target of ₹202, implying a modest upside of 5%. Module production is expected to increase significantly from 1,900 megawatts in FY25 to 7,716 megawatts by FY28, with revenue, EBITDA, and profit after tax projected to grow at compound annual growth rates of 50%, 59%, and 71%, respectively.

| Cos/ | Rating/ | TP/ | Upside/Downside |

|---|---|---|---|

| Waaree Energies | Reduce | ₹2,815 | 10% downside |

| Premier Energies | Reduce | ₹816 | 10% downside |

| Emmvee Photovoltaics | Buy | ₹291 | 31% upside |

| Vikram Solar | Add | ₹202 | 5% upside |

Sector outlook

JM Financial said that despite multiple announcements of integrated facilities, several projects may face delays or may not materialise due to capital and execution constraints. This could gradually lead to an oligopolistic market structure.

The brokerage also flagged that earnings for many manufacturers may have already peaked due to overcapacity and sectoral headwinds. Increasing pricing pressure and diversification into areas such as energy storage, rather than strengthening core operations, could weigh on margins and limit value accretion, potentially leading to industry consolidation over time.

Shares of Waaree Energies, Premier Energies, Emmvee Photovoltaics, and Vikram Solar were trading higher by up to 3.5% on Friday.