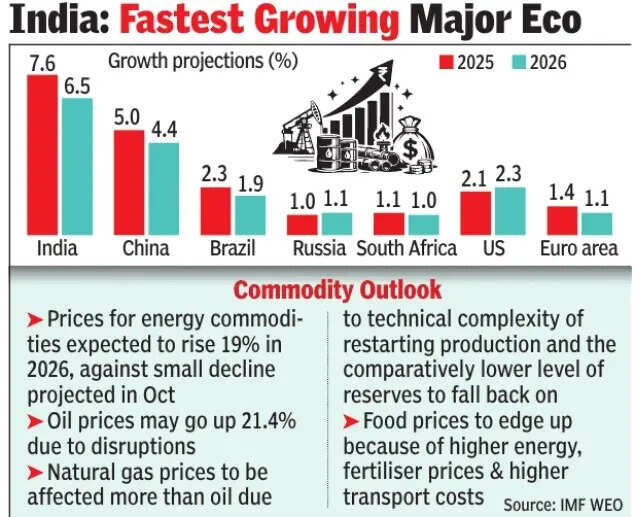

India’s high growth and low inflation period has been dealt an oil shock. Since the start of the Middle East conflict and US-Iran war, crude oil prices have crossed $100 per barrel, in effect threatening the growth story of major economies around the world. India is not immune to the shock, especially as it has high import dependency when it comes to energy needs. However, agencies like IMF and S&P Global have expressed confidence in India’s fundamentals to tide over the current crisis.In its latest World Economic Outlook report for April 2026, IMF has actually raised the growth forecast for India in the ongoing financial year to 6.5%. The raise comes as a result of favourable effects of last year’s high growth numbers and the lowering of US tariffs, which IMF argues will help more than offset the impact from the Middle East crisis.S&P Global in its latest report titled India’s Strong Fundamentals Would Cushion The Blow Of An Oil Shock says India is equipped to handle some strain.

The report assumes a base case scenario of oil prices at an average of $130 per barrel for 2026 and $100 in 2027. This scenario assumes that the war’s intensity will peak and the Strait of Hormuz’s effective closure will ease during April, but some disruptions will likely persist for months.

The Oil Shock Impact

“India isn’t immune to the shocks reverberating from the Middle East war. The pain of higher energy prices and supply disruptions may persist for months, crimping economic activity across households, corporations, and banks,” the report says.S&P Global explains how an oil price shock will transit itself into the Indian economy through mainly four channels. These are:

- The current account balance weakening

- Higher input costs for producers which will result in margins getting squeezed

- In turn, higher prices for consumers will mean reduced purchasing power

- When the government will step in to absorb the price shock for consumers, it will strain finances

What is important to understand is that oil is fundamental to several sectors and any domestic energy source substitution will take time, the report says. To put simply, oil’s role in downstream chemicals heightens its economic influence. “Energy supply disruptions that lead to fuel rationing or shortages of downstream petrochemicals and related products such as fertilizers are a risk that could hamper growth,” says S&P Global.

Rising oil prices mean that the current account balance will deteriorate with higher import costs. “Widely used estimates from the Reserve Bank of India and market research suggest that a sustained price increase of $10 per barrel lead to about 0.4 percentage points widening of the current account deficit as a share of GDP,” the report notes.Rupee, which has already depreciated around 3% year-to-date, also comes under pressure. With likelihood of sustained risk-off flows, S&P Global expects the rupee to continue depreciating during the year.Where the shock begins to hit is when it impacts household budgets. “An energy shock would also reverberate through the economy as prices rise. Input costs for producers would increase and squeeze margins and output. Higher prices would eventually be passed on to consumers, weakening their purchasing power,” the report explains the transmission.Finally, from a government point of view, spending would see a shift towards subsidies as it looks to protect the common man from the price rise. This means that fiscal consolidation plans may take a back seat.“A weaker fiscal position resulting from higher subsidy spending will curtail demand in the public sector. Uncertainty could harm confidence for the private sector, and the external balance would be strained. Gains in food prices would likely be gradual, and the large agricultural sector could face fertilizer shortages. Similar constraints are likely across different parts of the economy. For example, gas is rationed in certain sectors. For now, the government has cut excise duties on fuel and kept prices at the pump relatively stable,” S&P Global elaborates.The excise duty cuts and fertiliser subsidies could strain finances, resulting in the government missing its 4.3% fiscal deficit target, the report cautions.However, S&P Global is confident that even though government measures to mitigate high energy prices may lead to a higher fiscal deficit, they will not derail India’s political commitment to fiscal consolidation over the next few years.Will the inflationary pressures mean that RBI will then hike rates to keep it in check? S&P Global expects any tightening to be modest. The economy entered calendar 2026 with strong growth momentum, resilient domestic demand, and contained inflation. But under a sustained energy shock, S&P Global expects economic growth to notably slow down.

What Will Save India?

S&P Global is of the view that India’s strong external position, a key strength in its sovereign credit profile, offsets the risks. “The country holds a net external asset position. While we forecast deficits for the current account will remain small over the next two to three years, they are likely to increase this fiscal year. A higher import bill and decreased remittances from the Middle East diaspora will drive the rise. This may temporarily leave India with a modest level of net external debt. However, we forecast its external balance sheet will continue to support the sovereign rating,” it says in the report.

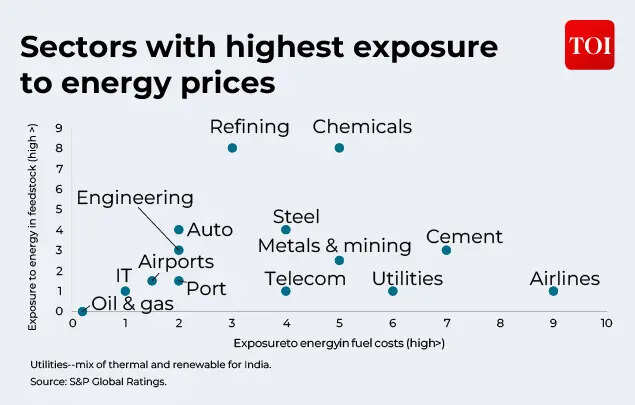

On the corporate front, S&P sees the EBITDA being hit across several sectors but sees resilience. “ At an aggregate level, we estimate that the EBITDA of about 100 of the largest corporates by EBITDA could decline by about 15% over fiscal 2027 and 10% over fiscal 2028 in our stress scenario, compared with previous expectations,” says S&P Global.If the disruptions extend up to six months, the resulting decline in capacity utilization, would mean that the corporate leverage increases by about 1x EBITDA in fiscal 2027. “Our scenario analysis shows a sharp rebound in earnings in fiscal 2028, with EBITDA recovering to fiscal 2026 levels. With most corporates entering the stress with strong balance sheets, it prevents a more severe deterioration in credit quality. Leverage at the end of fiscal 2028 would still be low relative to historical levels,” the report says. According to S&P Global, at a sectoral level:

- Chemicals, refining, and airlines are among the most exposed sectors.

- Cement, metals and mining, steel, and autos could also see material hits, either due to the high energy intensity or raw material pressures.

- The pharmaceutical sector may also face margin strains and supply chain risks. This sector, however, benefits from low leverage.

- The infrastructure sector, on the other hand, would be relatively unaffected.

- Utilities could see higher coal prices, but these would be passed on to customers under pricing mechanisms.

- Airports could see lower passenger traffic, particularly if fuel supply issues affect airline capacities.

Some of the other factors that work in favour of corporates are:

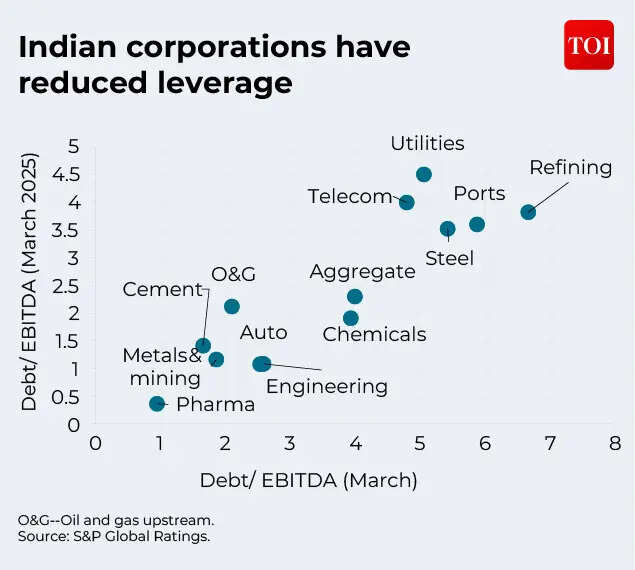

- The leverage of most sectors remains below the level at which Indian corporations entered the operational disruptions in 2020.

- Earnings have grown about 50% over the past five years for the largest corporations. Over the same period, debt grew 10%.

- Indian companies also have no major liquidity difficulties over the next year, in S&P’s view.

- Proactive refinancing means there are no major maturity walls for companies. Onshore liquidity and access to diverse funding sources underpin the liquidity positions of companies. In contrast, refinancing risk was an issue for many companies and strained credit profiles during the pandemic.

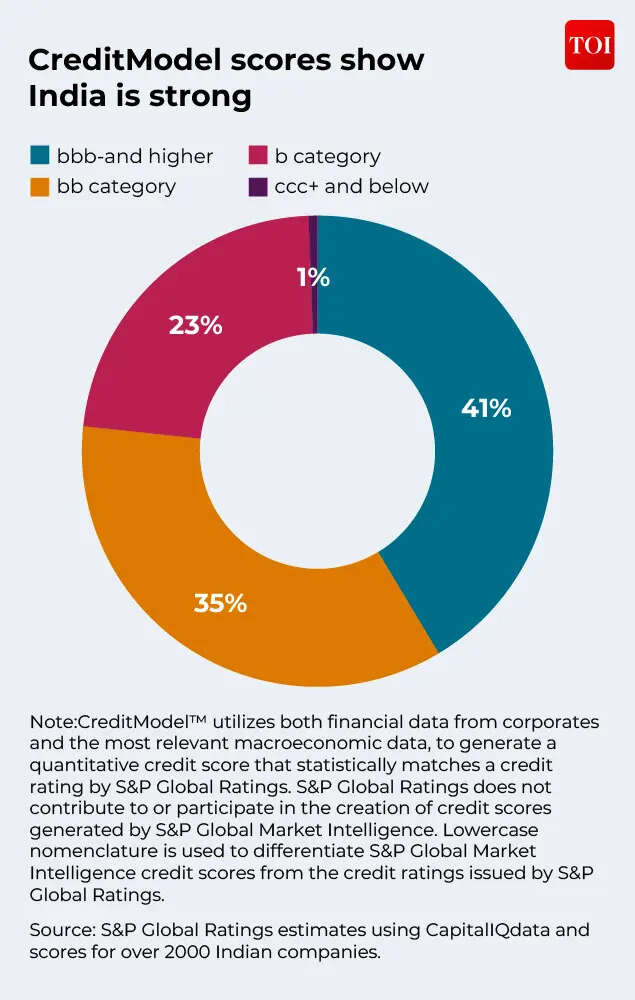

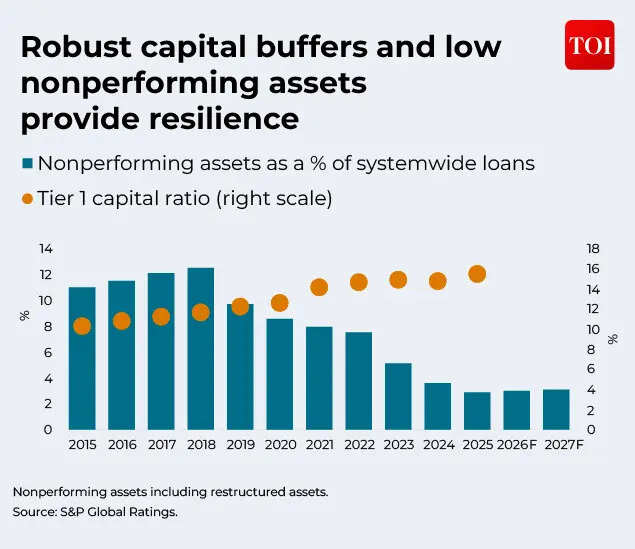

Yet another factor that will work in favour of India’s underlying economic strength is the banking system. As per S&P Global’s report, Indian banks are well-positioned to navigate elevated oil prices and a weakening rupee. “We believe sustained high energy prices and prolonged disruptions to global supply chains could weaken corporate and SME balance sheets. This could lead to a deterioration in asset quality for banks. However, the banks are starting from a position of strength, supported by near decade-high capital adequacy and multi-year low nonperforming loans,” it says.Any supply side shock would transmit to borrowers’ creditworthiness. However, banks do not have high exposure to chemicals, refining, and airlines, says S&P, pointing out that these are the sectors that are likely to be the most affected by the ongoing crisis. Not only that, the exposure of banks to other sectors that are exposed to energy shocks – cement, steel, and metals and mining – is also limited.

Add to that the point that strong fertilizer availability means there is near-term support to agriculture. However, a prolonged conflict may cause disruption to the next sowing cycle, prompting likely subsidy support from the government, the report says.“Higher fuel and transportation costs would squeeze real disposable income, with second-order effects on food and essential goods. Stress is likely to emerge first in unsecured segments and among self-employed borrowers. This could spill over to a degree into vehicle loans and affordable housing. However, the effects of retail issues should remain moderate for banks unless the shock becomes prolonged and begins to materially affect employment conditions,” the report adds.“The profitability of the Indian banking sector will be tested in fiscal 2027 not by domestic fundamentals, but by its ability to absorb external supply-side shocks., The combination of robust starting capital positions, a flight to quality for top-tier banks, and potential regulatory intervention suggests that the sector can avoid any sharp deterioration,” it concludes.

The Prolonged Crisis Scenario:

Even as S&P Global expresses confidence in India’s economic fundamentals it cautions that a longer conflict between the US and Iran could mean greater stress for India, as would be the case for most countries.“India would not be able to fully mitigate the damage of a sustained oil price shock. It is, however, in good shape to weather a few months of higher costs and supply-chain strain. We are watching for signs of how fast India can regain momentum in a scenario in which a ceasefire between Iran and its adversaries lasts. However, if hostilities again erupt, our focus will be on the measures that companies and the government take to prevent the crisis,” says S&P Global.