He also emphasised a continued focus on profitability and product mix, with margins guided at 26–28% and a gradual shift away from unit-linked insurance plans (ULIPs) towards protection and other segments. This balanced approach is aimed at sustaining long-term growth while improving business quality.

Watch the full conversation here or scroll for edited excerpts.

In the January-March quarter of 2026 (Q4FY26), SBI Life Insurance reported a mixed performance. New business premium rose 20% year-on-year (YoY) to ₹11,220 crore from ₹9,320 crore. Total annual premium equivalent (APE) increased 5.5% to ₹5,750 crore, while retail APE grew 7.4% to ₹5,220 crore.

However, the value of new business (VNB) declined 1.8% to ₹1,630 crore from ₹1,660 crore.

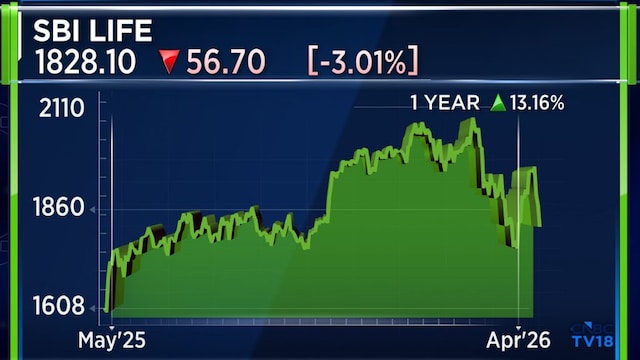

The company’s market capitalisation stands at around ₹1,83,209.76 crore, with its shares gaining nearly 14% over the past year.

These are edited excerpts from the interview.Q: What led to the moderation in margins, and what will drive growth going ahead?

These are edited excerpts from the interview.Q: What led to the moderation in margins, and what will drive growth going ahead?

A: We are happy that we have delivered numbers both on the topline and bottom line in line with the guidance provided at the start of the financial year (2025-26 – FY26).

There are month-to-month and quarter-to-quarter variations, but the overall annual performance is in line with our guidance. The first half was weak, while growth picked up after August, particularly in September.

The October-December quarter of 2025 (Q3FY26) was strong, while the January-March quarter of 2026 (Q4FY26) was slightly weak, partly due to geopolitical events. However, we are confident that despite these variations, we will continue to deliver as per expectations going forward.

Q: How has the start of FY27 been, especially in April?

A: It has only been a few weeks into the month, and April is generally a weak season. But as of now, we are seeing decent growth compared to February.

Also Read: HDFC Life, SBI Life and Max Financial now on similar footing, Bernstein cautious on PB Fintech

Q: What growth are you expecting for FY27?

A: For FY27, we are targeting around 14% top-line growth. We will also make every effort to grow above the industry average, which we have been doing for several years.

Q: What is the margin outlook and value of new business (VNB) guidance?

A: Our focus has always been on growth with profitability. We had guided for 26–28% margins last year and delivered within that range.

For the current year as well, we are maintaining the same guidance of 26–28% and are confident of achieving it.

Q: ULIPs and savings have been under pressure. What is your outlook?

Q: ULIPs and savings have been under pressure. What is your outlook?

A: We have not seen any major issues across product lines. Our focus has been on improving the product mix.

ULIP growth was around 6%, lower than overall company growth, but this is in line with our strategy to diversify into other segments.

Also Read: Quant MF finds value in insurance, wealth after correction; avoids oil plays

Q: How are you planning to change the product mix in FY27?

A: We aim to improve the product mix by 3–4 percentage points. ULIP contribution has already reduced from 70% to 66%, and we are targeting around 63% this year.

The shift will be towards protection, non-par and participating segments.

Q: What is the outlook for protection and annuity segments?

A: Protection remains a key focus, and we have seen strong growth of 23% in the last financial year.

Annuities also offer significant opportunities, given the need for retirement savings. We will continue to focus on these segments and expand the number of policies.

Catch all the latest updates from the stock market here