Balachandran said the company’s core business fundamentals remain unchanged, with the combined ratio expected to stay within its historical 102–103% range, excluding market-wide events. He also expects growth momentum to remain healthy across key business segments, supported by strong on-ground demand.

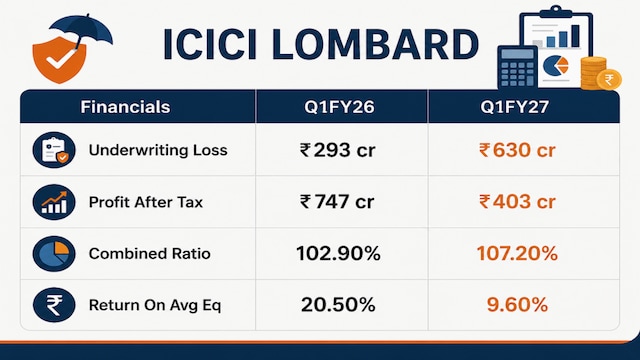

ICICI Lombard’s comments come after the insurer reported a 46% year-on-year decline in net profit to ₹403 crore for the April-June quarter of 2026 (Q1FY27), compared with ₹747 crore a year earlier, as exceptional items weighed on earnings. However, net premium earned rose 15.9% year-on-year to ₹5,950 crore, up from ₹5,136 crore in the corresponding quarter last year, reflecting continued growth in its core insurance business.

Mumbai-based ICICI Lombard General Insurance Company has seen its shares decline nearly 19% over the past year and currently has a market capitalisation of around ₹80,192.35 crore.

This is an edited transcript of the interview.Q: Let’s address the one-offs first. There were two large fire claims and the impact of the Supreme Court judgment on motor third-party reserves. What would your underwriting loss, operating profit and combined ratio look like if these one-offs are excluded?A: Before I respond to your specific question, let me put this in context. The core of our underwriting philosophy remains unchanged. We will continue to underwrite profitable risk selection. That’s something we have always followed and will continue going forward.

Coming to the specific events, on the fire business, there were two large losses that impacted our combined ratio by about 1%.

Then there was the Supreme Court judgment in June. Motor third-party portfolios inherently get impacted by court judgments from time to time. We have seen similar situations earlier as well. The most recent example was in 2021, when there were a couple of judgments affecting the industry.

Based on our preliminary assessment, we believe this judgment will increase the motor third-party loss ratio across the industry by 12–15%.

As always, we have taken a prudent and conservative approach. After assessing our exposure, we have taken a ₹165 crore charge in the first-quarter numbers.

If you exclude both these events, our combined ratio for Q1 would have been 102.3%, compared with 102.2% in the same quarter last year. So, our core business fundamentals remain intact. The Supreme Court judgment is an industry-wide event, and its impact will play out across the market.

Q: What happens now? Has the industry sought a review of the Supreme Court judgment? Secondly, where do you expect loss ratios to settle this year?A: Over the last four to five years, the motor third-party business has not seen any meaningful price revision. Coupled with this judgment, we believe there is now a strong case for an industry-wide price increase, which would be positive for the sector as well as for us.

Secondly, the General Insurance Council, representing the industry, has filed a review petition. We will wait to see the outcome.

Beyond that, there are operational efficiencies that we can continue to create, and that is something we have always worked on and will continue to focus on, including in the motor third-party portfolio.

The combined ratio is also influenced by management expenses. We will continue to optimise sourcing costs and operating efficiencies.

There are several moving parts, so we will closely monitor developments over the coming quarters. However, our long-term objective remains unchanged — to deliver a ROE of 18–20%.

Q: You mentioned the judgment strengthens the case for higher motor third-party premiums. Are we looking at a double-digit price increase? What’s the timeline?A: As I mentioned, there has been no meaningful price revision over the last four to five years.

Q: You mentioned the judgment strengthens the case for higher motor third-party premiums. Are we looking at a double-digit price increase? What’s the timeline?A: As I mentioned, there has been no meaningful price revision over the last four to five years.

Our preliminary assessment suggests the judgment will increase motor third-party loss ratios by 12–15%. Naturally, the industry’s expectation would be to seek a price increase of a similar magnitude.

The timing will depend on the regulator, since third-party premiums are tariff-driven.

At the same time, insurers will continue improving operational efficiencies. At ICICI Lombard, our management expenses are already well within the 30% regulatory limit, although we continue to look for further efficiencies. There are players operating with much higher expense ratios, so the industry will have to recalibrate accordingly.

Q: Moving to corporate health, underwriting losses have increased sharply. What caused this, and is it likely to continue?A: We have always differentiated between corporate health and retail health.

For corporate health, we are comfortable with a mid-90s loss ratio, while for retail health, our preferred range is 65–70%.

This quarter, the corporate health loss ratio was elevated at around 89%, while retail health was around 66%, which is well within our target range.

Across the industry, we have seen higher claim incidences in corporate health during the first quarter. Normally, this trend appears in the second quarter because of the monsoon. This year, it has come earlier.

We will continue to monitor how this develops and focus on improving claims management efficiencies.

Q: Can you give us a sense of your FY27 premium growth outlook and where the combined ratio could end the year?A: We are in the business of managing risk, so it’s difficult to predict unknown future events.

Q: Can you give us a sense of your FY27 premium growth outlook and where the combined ratio could end the year?A: We are in the business of managing risk, so it’s difficult to predict unknown future events.

However, our business philosophy remains unchanged. We will continue writing profitable business while closely monitoring combined ratios.

Over the long term, we remain committed to delivering a ROE of 18–20%.

Q: Can you give a number for the combined ratio by the end of FY27?A: At this stage, these are market-wide events, so we need to see how developments unfold.

Leaving aside such extraordinary events, we continue to target a combined ratio within our historical 102–103% range.

It’s also important to note that the industry’s combined ratio has worsened by nearly 500 basis points compared with 2024-25 (FY25) and 2025-26 (FY26), and that context should be kept in mind while assessing our performance.

Watch the full conversation here

Q: Your net earned premium grew around 16% in the first quarter. Can that pace continue through the rest of the year?A: The momentum across our business lines remains very encouraging, whether it’s corporate health or motor.

We have already started seeing early signs of this. In June, we outperformed across all three key segments.

We will continue to watch how the market evolves, and that will determine the trajectory of our earnings going forward.

Catch all the latest updates from the stock market here