Englander expects the Indian rupee to remain broadly around current levels of 96–97 against the US dollar, saying there is no significant upside for the currency over an extended period. He also believes softer US inflation data is more important for the Federal Reserve’s policy outlook than the recent rise in energy prices.

This is an edited transcript of the interview.Q: When it comes to currencies, we’ve seen significant capital flows, outflows towards artificial intelligence and geopolitical uncertainty. What’s your call on the dollar and the rupee?

A: In some ways, the dollar is the easier call because the strength in productivity, the uniqueness of the US position in the artificial intelligence (AI) world and the strength of US earnings will continue to attract capital to the US. At the same time, they will push up equilibrium interest rates, not because of inflation but because of the high returns on investment.

We think that is going to be dollar-positive over the medium term, as long as those investments continue to generate the returns we expect and the US stays ahead of other countries. It could actually be one of the biggest positives for the dollar.

The rupee is more complicated. Like many other countries, India is not at the forefront of AI right now, although it may get there. Energy prices are elevated and there is a lot of uncertainty. In the short term, the market may well be too short on the rupee, but we don’t see any significant upside for the currency over an extended period.

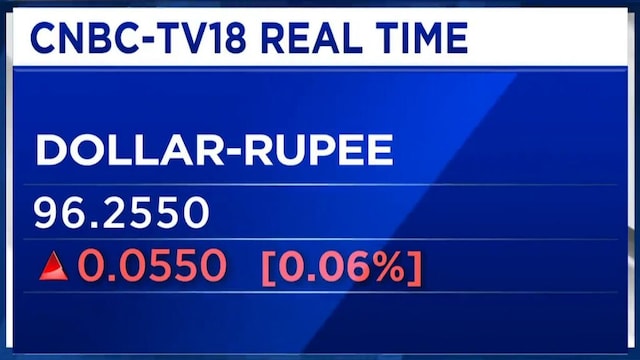

Q: The rupee closed at 96.6 against the dollar yesterday and is around 96.25 now. Just when we thought the worst of the depreciation was behind us, the latest macro shock pushed the rupee down again. Do you have a level for the Indian rupee?

A: Over the medium term, we see it roughly around current levels, about 96–97 against the dollar, not very different from where it is now.

Q: We have had two soft US inflation prints, with both Consumer Price Index (CPI) and Producer Price Index (PPI) undershooting expectations. With crude oil prices rising, does that feed into headline inflation? And what does the Fed do next?

A: I think the US is different from most countries. There isn’t an automatic assumption that higher energy prices will feed through into core inflation for an extended period.

The fact that CPI, and the components of PPI that feed into Personal Consumption Expenditures (PCE), are coming in on the soft side is more important for the Fed’s rate outlook. Historically, the US economy has absorbed energy price shocks through weaker demand rather than through persistently higher inflation. That’s less true in Europe and much of the rest of the world.

The market focused on the softer inflation numbers. Maybe it interpreted them a little too literally, but that is what investors were looking at. They assumed the pressure on the Fed had eased, the dollar weakened a bit, although we think that’s temporary, and equity markets rallied significantly. It’s a different response from what you see elsewhere.

Q: The Bank of Korea has just raised rates for the first time in more than three years, by 25 basis points to 2.75%, citing inflation above its 2% comfort level. Does this have any implications for capital flows or the Korean won, especially since Korea seems to be moving differently from India?

A: The won has appreciated quite significantly over the last couple of weeks. A lot of that is because markets have been unwinding hedges they no longer want to hold. I don’t think it’s a fundamental issue.

Watch the full conversation here

The Korean authorities have shown that they are very concerned about currency weakness, even at current levels. They don’t want the currency to become a one-way bet, and I think that’s true for many emerging economies.

Even if domestic inflation isn’t particularly threatening, they can’t afford to let the exchange rate or energy prices lose credibility. That’s why they hike rates, while the Fed doesn’t.

Catch all the latest updates from the stock market here