Jefferies has a “buy” recommendation on the stock with a price target of ₹180 per share, indicating an upside of 11.9% from Friday’s closing levels.

The brokerage has raised its estimated earnings per share (EPS) for FY27 by 20% and for FY28 by 29% on a sharp reduction in depreciation rate.

GAIL’s fourth quarter earnings before interest, tax, depreciation, and amortization (EBITDA) was a sharp miss compared to the brokerage and consensus estimates on weakness in gas trading and the petchem business, according to Jefferies.

Jefferies said that it has raised its earnings estimates for GAIL, despite a “lost opportunity” from the power sector demand this summer due to the West Asia crisis. However, hopes remain pegged on a quick resolution to the conflict.

As a result, Jefferies has lowered GAIL’s EBITDA estimates by 8% for FY27 and left its expectations for FY28 broadly unchanged.

Among the 33 analysts who have coverage on the stock, 26 have a “buy” rating, six have a “hold” rating and one has a “sell” rating.

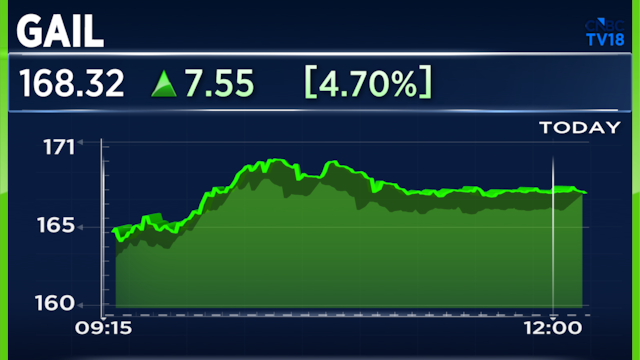

Shares of GAIL are trading 5.1% higher on Monday at ₹169. The stock is up for the third straight day and has nearly recovered all of its losses for 2026.

Also Read: Sterlite Tech shares extend 2026 gains to 352% after bagging a $1.1 billion contract