While the Street had expected a largely flat quarter amid a moderation in market activity after a strong March quarter, Groww reported revenue that was broadly in line with estimates and earnings that exceeded expectations.

Revenue remained largely flat sequentially at ₹1,501 crore. EBITDA rose 4% quarter-on-quarter to ₹963 crore, while margins expanded by more than 200 basis points as an 11% decline in other expenses and operating efficiencies more than offset a 5% increase in employee costs.

Lower operating expenses and higher other income also helped profit after tax rise to ₹735 crore, beating expectations of a largely flat quarter.

How brokerages reacted to Groww Q1

JPMorgan reiterated its ‘Overweight’ rating on the stock and raised its price target to ₹250 per share. The brokerage said Groww delivered revenue in line with expectations but posted a sharp beat on EBITDA and earnings per share. Revenue increased 66% year-on-year, while EBITDA came in 6% above its estimates.

The brokerage said growth was driven by the margin trading facility (MTF) business, where revenue surged 335% year-on-year, followed by equity and commodity derivatives at 65% and cash equities at 39%. Total transacting users increased 24% year-on-year, while customer assets rose 38%.

JPMorgan also highlighted that EBITDA margin expanded 230 basis points sequentially to 64.6%, aided by operating leverage.

Jefferies retained its ‘Buy’ rating and also raised its price target to ₹250. The brokerage attributed the EBITDA beat to lower operating expenses and noted that Groww’s revenue mix continues to diversify. The contribution from options trading declined to 52%, while newer businesses such as MTF, commodities and wealth management accounted for 14% of revenue.

Jefferies believes the planned launch of US stock investing later in FY27 could add another 5-9% to FY28 earnings.

While regulatory changes remain a key risk, it said the company expects only a limited impact from the recent RBI measures. The brokerage said that the stock trades at around 45 times FY27 estimated earnings, supported by an expected three-year EPS CAGR of 30%.

Motilal Oswal reiterated its ‘Buy’ rating and raised its price target to ₹250. The brokerage largely maintained its revenue estimates, with lower cash market and derivatives revenue offset by stronger-than-expected MTF income.

It also increased its FY27 and FY28 earnings estimates by 1% and 3%, respectively, citing improved operational efficiency.

Motilal Oswal said that weakness in equity derivatives was offset by higher activity in commodities, cash equities and continued strength in the MTF business.

It also highlighted that Groww’s cash market share declined by 0.7 percentage points due to deliberate risk-tightening measures, while loans against securities (LAS) now account for 30% of its lending portfolio.

The brokerage also stated that Groww has received approvals from SEBI and the Competition Commission of India (CCI) for State Street Global Advisors’ strategic investment in Groww AMC to jointly develop cross-border investment products.

According to Bloomberg data, eight of the nine analysts covering Groww have a ‘Buy’ rating on the stock, while one has a ‘Hold’ recommendation.

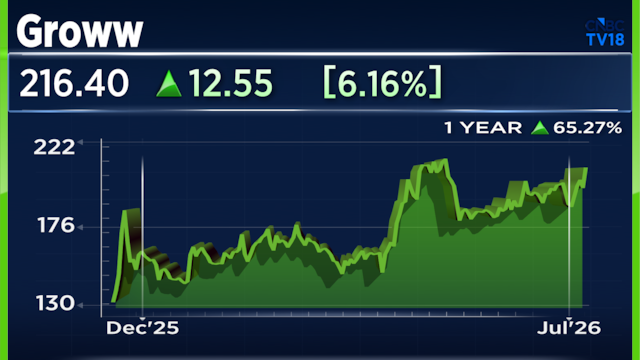

Shares of Groww ended 6.46% higher at ₹216.95 on Wednesday and have gained nearly 40% so far in 2026.