The company said it opened the financial year 2027 on a solid footing and it is expected to deliver a strong performance in the first quarter. Its business is expected to deliver growth around thirties in the quarter under review, led by continuous growth momentum across its focus categories, it said.

Honasa Consumer has estimated growth to be in the mid-twenties during the first quarter, on a reported basis, adjusting for the change in revenue recognition policy by the Flipkart group.

Honasa Consumer’s largest brand Mamaearth is set to deliver high-teens growth compared to the previous year, powered by increasing consumer affection and strengthening offline distribution, it said.

The company added that its younger brands continue their strong growth momentum as well and are expected to deliver growth in the early forties.

The company said its offline channel continued to be a key growth driver, with general trade and modern trade expected to sustain strong growth momentum, aided by improving direct distribution reach in general trade and strong in-store execution across both channels.

It said its online channel is also expected to deliver healthy growth over the April-June period.

Honasa Consumer said it expects the business to sustain its momentum delivering a double-digit operating margin in the first quarter, aided by operating leverage from scale.

In its investor day held on June 11, Honasa Consumer said that it is targeting revenue of up to ₹5,500 crore, with Mamaearth target set at ₹2,000 crore, Derma Co. at ₹1,500 crore as well over the next five years.

The company is also projecting margins to rise to over 15% during this period.

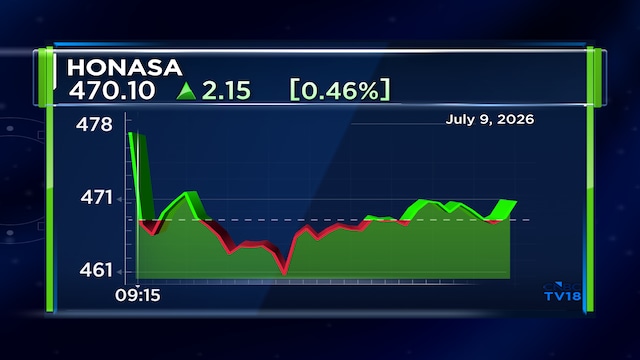

Shares of Honasa Consumer are currently trading at the flat line, having cooled off from the opening highs at ₹466.55. The stock has risen 65% so far in 2026.

Also Read: Explained – Why Jefferies is bearish on Dr. Reddy’s and Cipla but bullish on Mankind Pharma