Aziz also cautions that expectations of near-term rate cuts by the Federal Reserve may be misplaced. With inflation risks elevated and oil and labour markets still stable, he sees little room for rate cuts in 2026, and the possibility of rate hikes emerging instead unless a significant economic shock materialises.

Watch the full conversation here or scroll for edited excerpts.

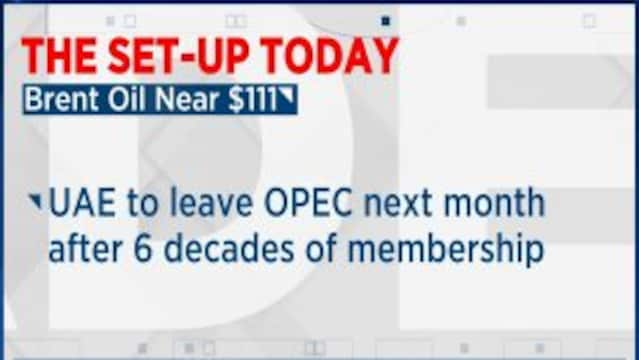

These are edited excerpts from the interview.Q: Let me begin with the United Arab Emirates (UAE) decision to exit the Organisation of the Petroleum Exporting Countries (OPEC) and OPEC+. What are the implications? Does this signal the beginning of the end for OPEC as we know it, and what happens to crude from here?

A: You are asking me questions I have no answers to. You have seen the public statement. Why the timing—well, I think that is best left in the public statement by the UAE. I really do not have any further insights into that.

Q: On the US-Iran situation—the stalemate continues, the blockade is stifling exports, and it’s gone on longer than expected. How do you see this playing out?

Q: On the US-Iran situation—the stalemate continues, the blockade is stifling exports, and it’s gone on longer than expected. How do you see this playing out?

A: That’s clearly the issue. We have an indefinite ceasefire, and the assumption was that negotiations would take place. Negotiations are probably happening indirectly through third parties rather than directly, which creates uncertainty about when and how this conflict will be resolved.

Positions on both sides are quite far apart. The market is gradually pricing in that this conflict may last longer than expected. As you pointed out, it has already lasted longer than expected since February. If you look at futures prices and dated Brent prices, both are creeping towards pricing in a longer shortage or stoppage in supplies, which is not good for oil prices or supply stability.

Also Watch | UAE exit from OPEC signals shift in global oil supply dynamics amid crude price surge

Q: This is hitting Asian economies more. Governments have been absorbing the shock, but with elections ending, will more of the burden be passed on to consumers?

A: That’s correct. If you go back to previous episodes of oil price shocks, the overall stance of governments has always been that everyone has to share the burden—it cannot be exclusively on the budget, individuals, or corporates.

That is more or less what is happening again. You can debate the timing, but the adjustment will be borne by corporates, the budget, and the exchange rate. This is how governments, both current and previous, have responded to oil price shocks.

Q: On the Fed—investigations against Jerome Powell have been dropped, and the path may be clearer for Kevin Warsh. Is this dollar-negative?

A: It is very hard to look at the oil price shock and current unemployment at 4.3% and say there is scope for rate cuts in the near term. We don’t have any rate cut for 2026; in fact, the next move by the Federal Reserve, to us, is a rate hike, possibly in 2027.

Unless there is a large negative shock to the economy—which does not seem likely—it is very hard to see rate cuts in the near term.

Q: Beyond interest rates, what is the consensus expectation on policy direction?

Q: Beyond interest rates, what is the consensus expectation on policy direction?

A: The consensus is that there are pressures on the Fed to cut rates, so some cuts are being priced in. But that keeps changing, and the mean of the distribution does not clearly point to rate cuts.

The chair is just one vote and needs broader support within the Federal Open Market Committee (FOMC). Looking at fundamentals, it is very hard to argue for rate cuts. If you look at major central banks like the Bank of England or European Central Bank (ECB), they are not cutting rates—if anything, they are hiking or staying cautious due to inflation risks from oil.

At best, you can hope for is a hold from the FOMC for most of the year.

Catch all the latest updates from the stock market here