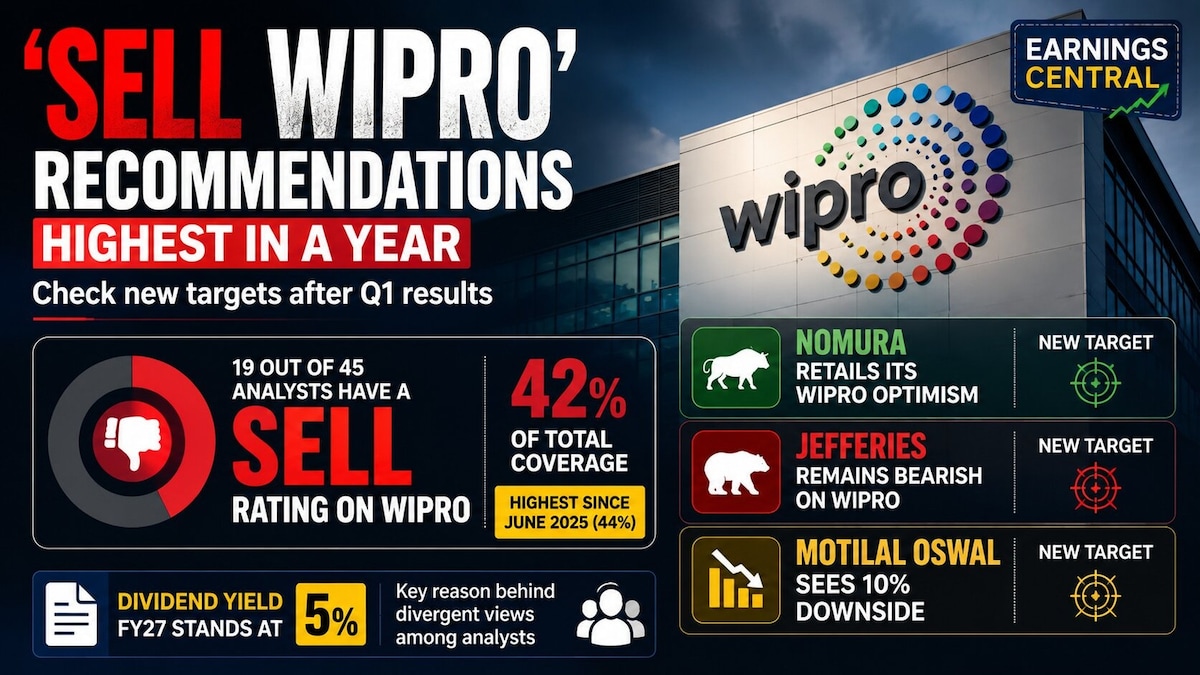

At the current price, Wipro’s dividend yield for financial year 2027 stands at 5%. It is this dividend yield that has led to a divergent opinion among both the bullish and bearish analysts on the stock.

Nomura Retails Its Wipro Optimism

Brokerage firm Nomura has maintained its “buy” rating on Wipro with a price target of ₹190. It called the first quarter a subdued one and its guidance for the second quarter to be below what it had anticipated.

The management only expects a return to the 17% to 17.5% margin band over a period of time.

It went on to say that the current 5% dividend yield should provide some support for the stock.

Jefferies Remains Bearish On Wipro

On the flip side, Jefferies has a price target on ₹150 on Wipro, which is among the lowest on the street for the stock. The brokerage has an “underperform” rating on the Bengaluru-based IT services provider.

Jefferies wrote in its note that the first quarter results and guidance for the September quarter were a key negative surprise.

“Wipro has struggled to grow organic revenues for three years and financial year 2027 is unlikely to be any different,” the brokerage said.

Therefore, it has cut its revenue estimate by 2% and profit estimates by 5% for the year to factor in a slower growth outlook.

The brokerage expects Wipro’s Earnings per Share (EPS) to grow at a Compounded Annual Growth Rate (CAGR) of 5% over financial year 2027-2029, which along with the 5% dividend yield, makes risk-reward very unattractive.

Motilal Oswal Sees 10% Downside

Motilal Oswal has a “neutral” rating on Wipro with a price target of ₹160.

The brokerage is also modelling another weak year for Wipro with constant currency revenue growth projected to be flat to slightly negative due to slower deal ramp-ups and an uneven recovery across verticals.

“We also expect margin recovery to remain gradual, as continued AI investments, the remaining wage hike impact in Q2, and deal ramp-ups offset operational improvements,” Motilal Oswal said.

As a result, the brokerage has cut its financial year 2027 EPS estimates by 3.5% to factor in the weaker-than-expected first quarter margin performance and a weaker growth in the first half.

How Did Wipro Fare In Q1?

Wipro’s margins for the first quarter were the lowest in nearly four years. The 16% figure was well below the 16.9% poll projection from CNBC-TV18 and the 17.3% it reported during the March quarter.

The revenue growth in the quarter stood at a negative 1.2% and has guided for the second quarter revenue growth to be between -1.5% to +0.5%. Analysts were projecting the growth figure to be between -2% to +2%.

Nine out of the 45 analysts who have coverage on Wipro have a “buy” rating on the stock, while 17 others have a “hold” rating.

Shares of Wipro had ended 1.8% higher on Thursday before the results announcement at ₹177.7. The stock is still down 35% so far this year.