Macquarie has upgraded Tata Motors PV to “outperform” from “neutral”, and it has increased its price target to ₹381 from ₹367 earlier.

The brokerage said the stock benefits from a favourable SUV launch cycle.

It views that the JLR margins should gradually improve in the ensuing quarters.

Benign stock valuations also sees Macquarie stating that there is downside protection for the stock.

It said the India passenger vehicles business earnings should improve with favourable model cycle-led market share gains.

On another note, earlier this month, the company reported higher production and domestic sales across most of its PV portfolio in the June quarter, as per data submitted to the Society of Indian Automobile Manufacturers (SIAM).

It said the production of its Punch and Nexon units rose to 11.77 lakh in the first quarter from 80,001 units in the year-ago period. The domestic sales of the models increased to 11.58 lakh units from 76,230 units, while exports were at 317 units in the first quarter compared to 320 units in the previous year.

A couple of days later, Tata Sons chairman N Chandrasekaran, at the firm’s 81st Annual General Meeting, said the company plans to launch six new car models and more than 20 product upgrades by FY31, as part of its target to grow its business tenfold over the decade from FY20-31.

The automaker is aiming for annual sales of more than 1.2 million vehicles by FY31, nearly double its FY26 domestic sales of approximately 6.42 lakh units, which was already the firm’s highest-ever annual figure.

It is also targeting a 20% market share, up from 14.2% in the most recent quarter, and a double-digit EBITDA margin.

Of the 32 analysts who have coverage on the stock, 13 have a “buy” rating, 10 have a “hold” rating and nine have a “sell” rating.

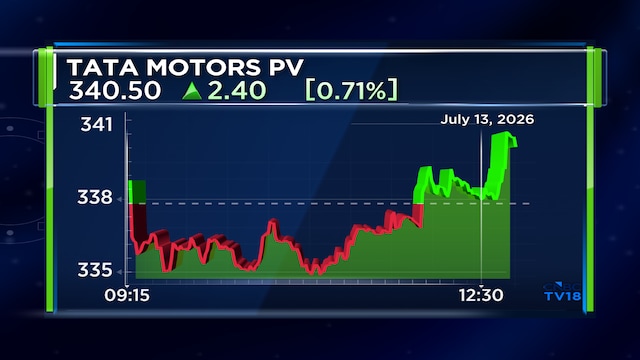

Tata Motors PV shares were trading 0.4% up at ₹339.3 apiece at 12.45 pm on Monday.

Also Read: TCS shares jump 6% after expanding two-decade partnership with ABB