Motilal Oswal has initiated coverage on Tata Capital with a “neutral” rating and a price target of ₹364 per share, which implies an upside potential of 7% from its earlier closing price last Thursday.

Motilal Oswal said Tata Capital represents a high-quality franchise with strong parentage, a granular and increasingly retail-oriented portfolio, and a demonstrated track record of execution.

While it expects the firm to deliver healthy assets under management (AUM) growth and gradual improvement in profitability over the medium term, it is of the view that the current valuations adequately reflect these positives.

The Motilal Oswal note said that a meaningful re-rating for Tata Capital would require sustained improvement in return on assets and return on equity and continued expansion in higher-yielding retail lending segments.

Tata Capital delivered a 29% AUM compound annual growth rate (CAGR) over financial year 2023-2026, reflecting the strength of its franchise, diversified business model and consistent execution, according to Motilal Oswal, who added that the company’s loan portfolio is highly granular, with 98% of its accounts having a ticket size less than ₹1 crore.

Asset quality is supported by a predominantly secured lending book, while the portfolio is also well diversified with no single product contributing over 20% of total loans.

Motilal Oswal believes Tata Capital is well-positioned to sustain a healthy AUM CAGR of 23% over financial year 2026-2028, with a calibrated shift toward high-yielding segments and continued investments in digital capabilities.

It said the company benefits from a strong liability franchise, supported by the Tata Group parentage and an AAA credit rating. This enables access to funding at competitive costs. Motilal Oswal said it expects margins to gradually improve as the portfolio mix shifts further toward retail and unsecured lending, with net interest margins (NIMs) estimated to increase to 5.4% and 5.5% in financial year 2027 and 2028 respectively, from 5.2% in financial year 2026.

The brokerage said Tata Capital has displayed disciplined cost control measures via digital initiatives, process improvements and branch-level productivity. As new branches scale and technology matures, its productivity gains are expected to enhance efficiency, it said.

Motilal Oswal said the company has consistently demonstrated prudent risk management via disciplined underwriting standards and proactive collection practices. While credit costs remained below 1% during FY23-24, they increased after the Tata Motors Finance Ltd merger, driven by elevated delinquencies in the captive vehicle finance business and stress within certain unsecured lending portfolios.

The company is now steadily turning around its Motors Finance business with the segment returning to profitability in the March quarter. Also, its unsecured segments are seeing sharp asset quality improvement, leading to moderation in credit costs, the brokerage said, expecting the same to moderate further to 1.1% in both FY27 and FY28.

The brokerage sees the following key risks for the stock:

- Margin pressure from intensitfying competition

- Higher-than-expected stress in the unsecured portfolio leading to elevated credit costs

- Slower-than-expected turnaround of Tata Motors Finance affecting profitability and return ratios.

Motilal Oswal has valued Tata Capital at 2.7 times its estimated March 2028 price-to-book value.

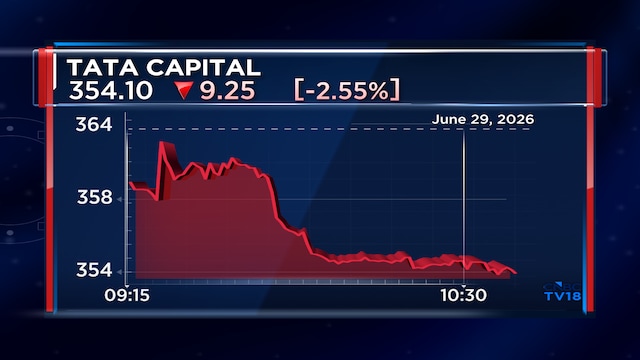

Shares of Tata Capital are trading 2.5% lower on Monday at ₹354.8. The stock is trading above its issue price of ₹326.

Also Read: Stocks To Buy: The top two AlcoBev picks highlighted by Jefferies for up to 25% upside