The reason, according to the global investment bank, has little to do with foreign investor flows or the artificial intelligence (AI) boom. Instead, it comes down to one factor that is currently separating Asia’s best-performing equity markets from the rest: corporate earnings growth.

While India’s long-term investment story remains intact, Goldman Sachs argues that South Korea and Taiwan are offering a stronger combination of earnings growth and valuations, making them more attractive markets for investors today.

Why foreign selling isn’t the real reason

Foreign portfolio investors have been persistent sellers of Indian equities over the past two years, fuelling the perception that global investors have shifted their attention almost entirely to North Asian markets.

However, Goldman Sachs argues that foreign flows alone do not explain why Korea and Taiwan have outperformed India.

According to Timothy Moe, Co-Head of Macro Research in Asia and Chief APAC Regional Equity Strategist at Goldman Sachs, overseas investors have sold nearly $100 billion worth of Korean equities so far this year—far more than the selling seen in either India or Taiwan. India has witnessed foreign selling in the mid-$20 billion range, broadly comparable to Taiwan.

The numbers suggest that market leadership has been driven by something more fundamental than capital flows.

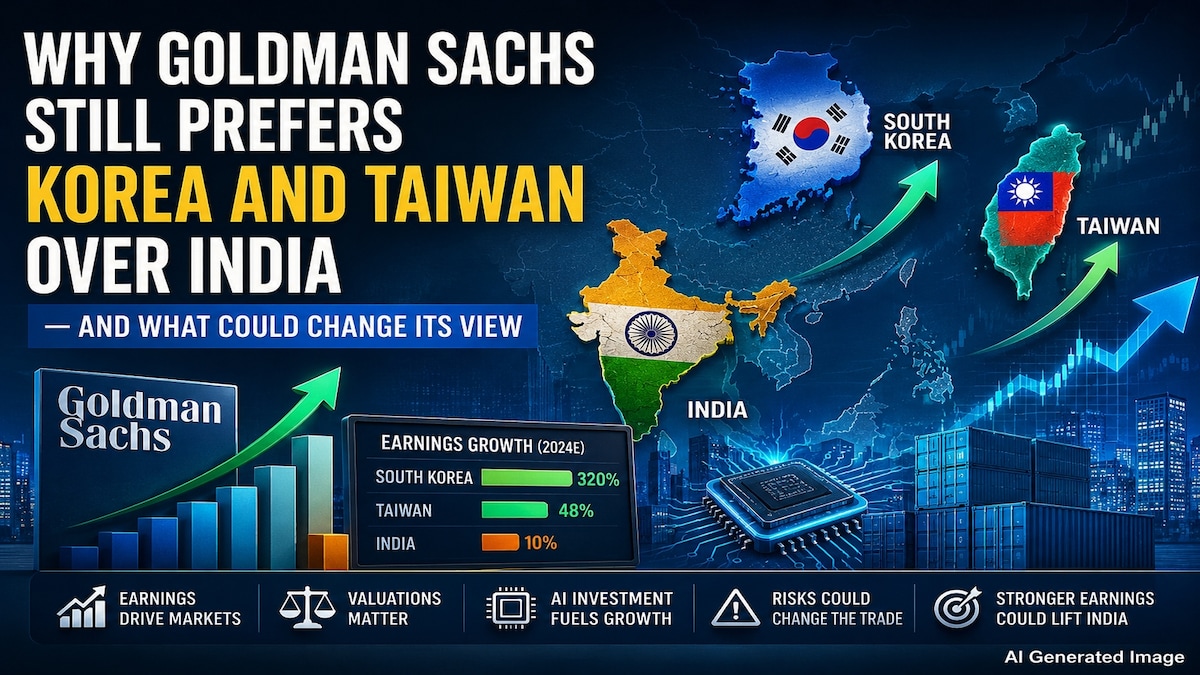

Earnings are driving market leadership

For equity markets, earnings growth remains one of the strongest drivers of long-term returns. Investors are generally willing to pay higher valuations for markets where corporate profits are growing rapidly and become less forgiving when earnings disappoint.

That is where Goldman Sachs sees the biggest difference between India and North Asia.

South Korea is expected to deliver an extraordinary 320% earnings growth this year—the strongest across the Asian markets covered by Goldman Sachs and among the highest growth rates the firm has recorded in decades.

Taiwan is expected to post earnings growth of around 48%.

India, by comparison, is forecast to deliver earnings growth of about 10% this year after Goldman Sachs recently raised its estimate from 8% as lower crude oil prices improved the earnings outlook.

As Moe told CNBC-TV18, “Markets are actually being very rational right now in rewarding where earnings are being delivered and being less focused, and less forgiving, in areas where earnings are falling short.”

That, more than any other factor, explains why Korea and Taiwan have outperformed India despite India’s favourable long-term economic fundamentals.

Similar valuations, very different growth

The comparison between India and Taiwan illustrates why earnings matter so much.

Both markets currently trade at broadly similar valuation multiples. India trades at around 20.5 times forward earnings, while Taiwan trades at roughly 21 times.

The difference lies in what investors are getting for those valuations.

Taiwan is expected to deliver earnings growth of about 48% this year and around 30% next year. India’s earnings are projected to grow by around 10% this year and 13% next year.

When valuation multiples are broadly similar, investors typically favour the market offering faster profit growth. That makes Taiwan’s risk-reward profile more attractive in Goldman Sachs’ view.

Why Korea stands out

South Korea presents a different investment case.

Despite its exceptionally strong earnings outlook, the Korean market trades at just 6.6 times forward 12-month earnings—close to levels last seen during the global financial crisis.

Some investors argue that Korean technology companies deserve low valuations because memory-chip earnings have historically been highly cyclical.

Goldman Sachs takes a different view. It believes the current AI investment cycle could prove more durable than previous technology cycles, allowing earnings to remain stronger for longer.

That combination of rapid earnings growth and inexpensive valuations is why the firm continues to maintain an overweight stance on Korea.

How AI is strengthening North Asia’s outlook

AI is central to Goldman Sachs’ positive view on North Asian markets because it is expected to sustain earnings growth across the region’s technology sector.

The firm estimates that demand for computing power could increase 24-fold by 2030 as AI applications evolve from today’s inference models towards more advanced agentic AI systems.

Meeting that demand will require enormous investment from the world’s largest technology companies.

Goldman Sachs expects hyperscalers to spend more than $1 trillion on AI-related capital expenditure next year, with much of that investment flowing through to semiconductor and hardware suppliers in Korea, Taiwan and parts of Japan.

Those economies occupy critical positions in the global AI supply chain, making them among the biggest beneficiaries of continued AI investment.

But the AI trade carries risks

The investment bank also believes investors should not assume the AI rally will continue uninterrupted.

Many hyperscalers are increasingly relying on debt and equity markets to finance their AI investments after using much of their excess cash.

If capital markets become less willing to fund those investments and AI spending slows, earnings expectations for technology companies could come under pressure.

Moe described such an outcome as “a negative surprise for the market”, saying investors would likely have to lower earnings expectations for AI-linked companies.

Ironically, such a slowdown could improve India’s relative appeal if domestic corporate earnings continue strengthening while North Asian technology stocks lose momentum.

India’s outlook is improving

Although Goldman Sachs remains market weight on India, its view has become more constructive in recent weeks.

Lower crude oil prices have eased pressure on India’s macroeconomic outlook, prompting the firm to raise its earnings growth forecast for the Nifty from 8% to 10%.

The rupee has also recovered, improving India’s relative attractiveness among higher-yielding Asian currencies.

Together, those developments have started to support Indian equities after a difficult period.

What would make Goldman Sachs more bullish on India?

Ultimately, the answer is straightforward: stronger and more sustained earnings growth.

Goldman Sachs uses the price-to-earnings-to-growth (PEG) ratio to compare markets. Korea and Taiwan currently enjoy lower PEG ratios because they combine faster earnings growth with more attractive valuations.

India’s earnings outlook is improving, but the investment bank wants more evidence that the acceleration can be sustained before upgrading its recommendation.

As Moe summed it up, “It really is all about earnings, and then, of course, valuation relative to earnings.”

For Goldman Sachs, the debate is not about whether India’s long-term investment story remains intact. The question is whether corporate earnings can accelerate enough to justify its relatively rich valuation. Until that happens, the firm believes Korea and Taiwan continue to offer a more compelling combination of earnings growth and valuations.