Despite the company’s recent fundraise and the sharp run-up in its stock price, Patil has maintained his ₹1,500 target price, citing strong growth prospects.

Patil expects Ather’s earnings profile to improve steadily as losses narrow, supported by capacity expansion, dealership additions and new product launches. “We are expecting the volume CAGR to be up at about 40–48% over next… till FY28, and we are expecting the company to gain market share close to about 20–22% by FY28,” he said.

He added that “in FY29 we are expecting the company to be PAT break even,” while also expecting further improvement in earnings before interest, taxes, depreciation and amortisation (EBITDA) margins.

The analyst said Ather remains one of the strongest players in India’s electric two-wheeler market. While the company is currently capacity constrained, he believes the ongoing expansion will support future growth. Ather is also expanding into new geographies, adding dealerships—particularly in northern India—and launching products in the affordable segment, which he believes will significantly expand its addressable market.

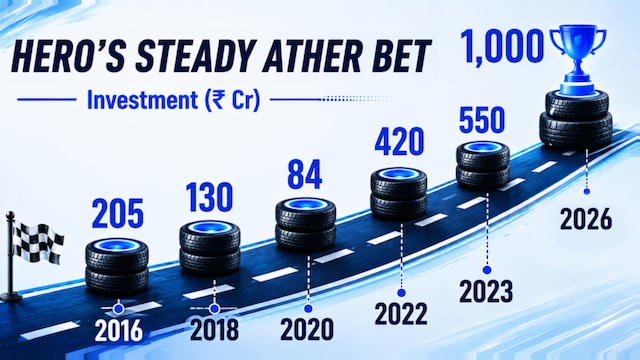

According to Patil, the company’s recent fundraise will primarily be used for capacity expansion, dealership expansion and product development, helping it strengthen its position in the Hero MotoCorp

(EV) market.

Despite Ather trading at around 5.8–6 times EV-to-sales, Patil believes the stock still has room for further re-rating. “We are giving about seven times EV to sales. So, that much steam is still left, I guess,” he said, adding that stronger EV policies and improvements in charging infrastructure could support further upside.

Patil also dismissed concerns that Ather’s growth would come at the expense of established two-wheeler manufacturers such as Hero MotoCorp and Hero MotoCorp. He said all major players continue to strengthen their EV businesses, making the industry more competitive rather than creating clear losers.

On Hero MotoCorp’s decision to increase its stake in Ather, Patil described it as a smart strategic move. He estimates it could add ₹400–500 per share to Hero MotoCorp’s sum-of-the-parts valuation and believes the partnership could create long-term synergies, including dealership expansion and a stronger presence in the EV segment.

Watch the full conversation her

On the India-UK Free Trade Agreement, Patil said it is broadly positive for the sector but believes it is still too early to assess its direct impact on individual companies, with domestic demand continuing to be the key growth driver for India’s two-wheeler industry.

Catch all the latest updates from the stock market here