“Ye tera ghar, ye mera ghar, ye ghar bohot haseen hai.” Owning that ‘haseen’ home has long been a cornerstone of the Indian dream. More than just a roof over one’s head, having one’s own home has traditionally represented stability, success and long-term security.But in 2026, that dream is running into a reality check. Property prices are climbing, rents are surging, and the cost of putting down roots in India’s cities is on a rise on all fronts. As homeownership slips further out of reach for many, millions of urban Indians are finding themselves grappling with a question that has never felt more relevant: should you buy a home, or is renting the smarter move?The first thing you need to ask yourself is: why am I buying a house? Is it an investment that you hope will yield good returns in the future? Is it an emotional need to own a home?The answer is becoming increasingly complex.

Renting that ‘jhilmil sitaron ka aangan’

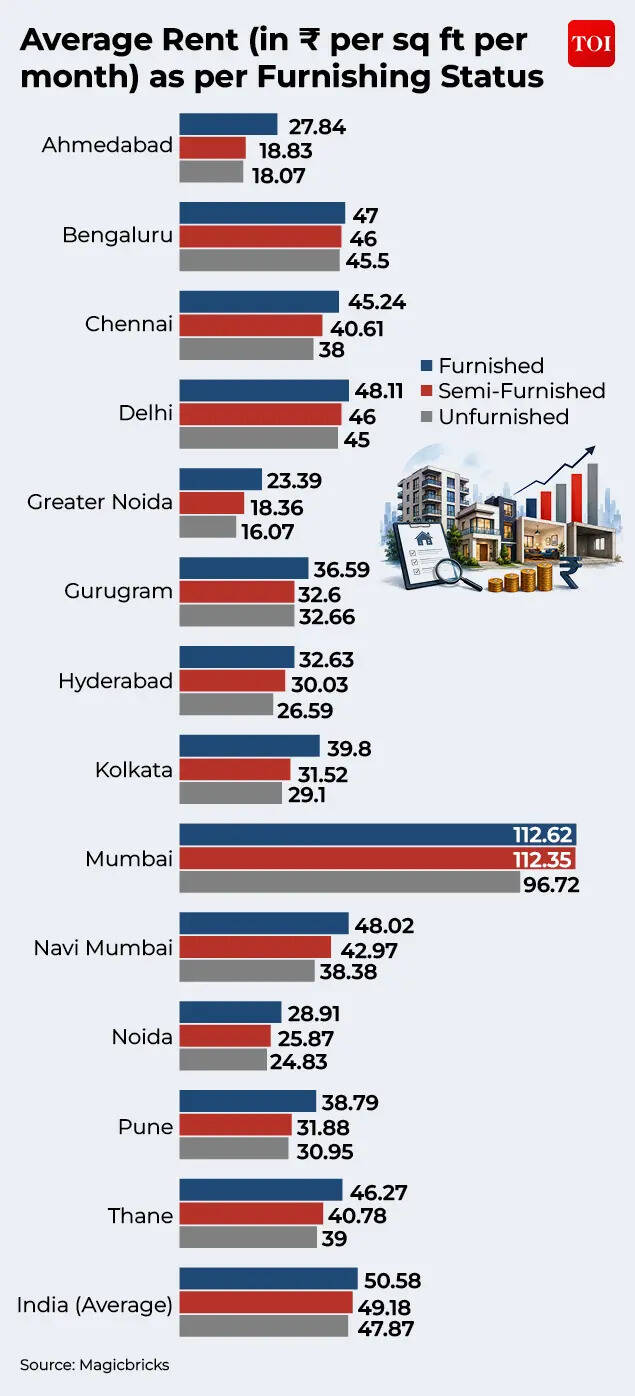

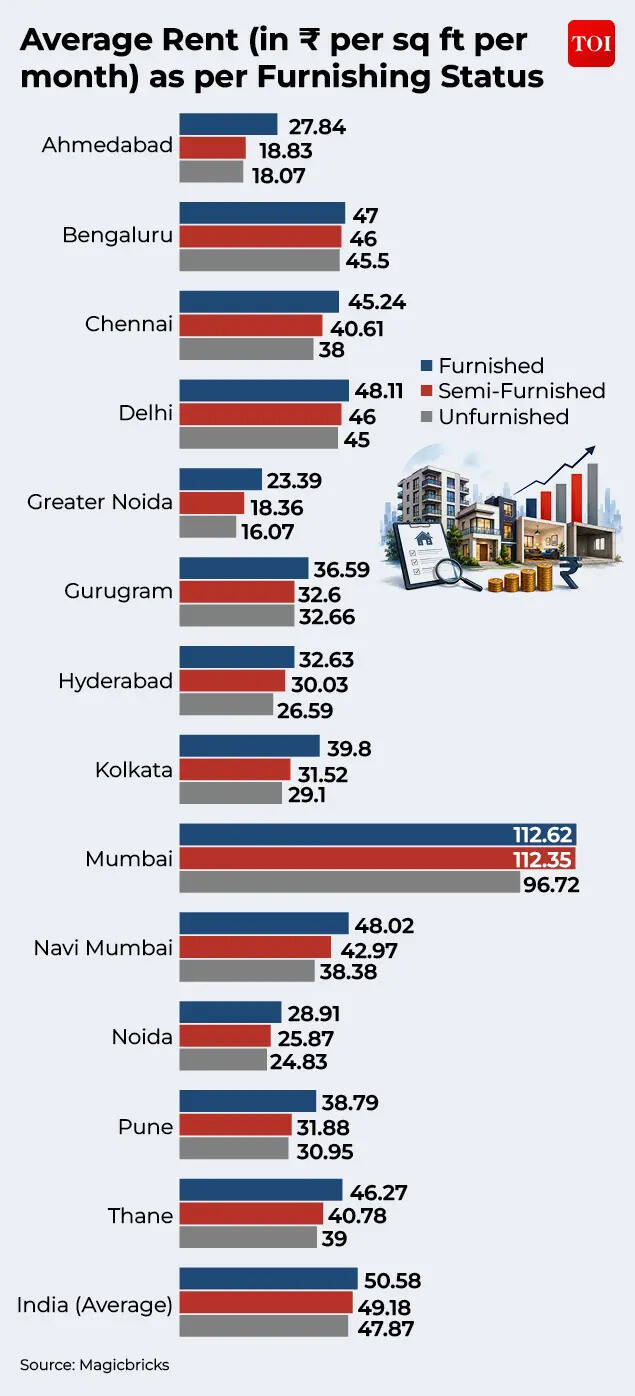

The rental market witnessed one of its strongest periods of growth in recent years during 2025.Property rents across Mumbai, Delhi, Bengaluru, Noida and Gurugram jumped by as much as 25%, driven by a combination of factors including rising property prices, return-to-office mandates, migration of high-income professionals and strong demand from corporate tenants.According to the Magicbricks Rental Index for January-March, average residential rents across India increased 14% year-on-year and 2% quarter-on-quarter.

Mumbai continues to be the country’s costliest city for renters. The city witnessed rent increases ranging from 1% to 20% across prime localities in 2025 as demand for larger homes with modern amenities intensified. According to the Magicbricks Rental Index, Mumbai remains India’s most expensive rental market, significantly ahead of other major cities. Although rental demand softened slightly in the January-March quarter, rents still increased 10.3% year-on-year.

Sapno ka mahal gets costlier

While tenants are left calculating their rising rents, prospective homebuyers face an equally challenging reality.According to a survey by Reuters, property experts suggest that home prices in India are expected to rise 6.3% during 2026 after already more than doubling over the past decade. Another Reuters poll projects average home prices to increase around 5% annually through 2028 as developers continue focusing on premium and luxury housing.

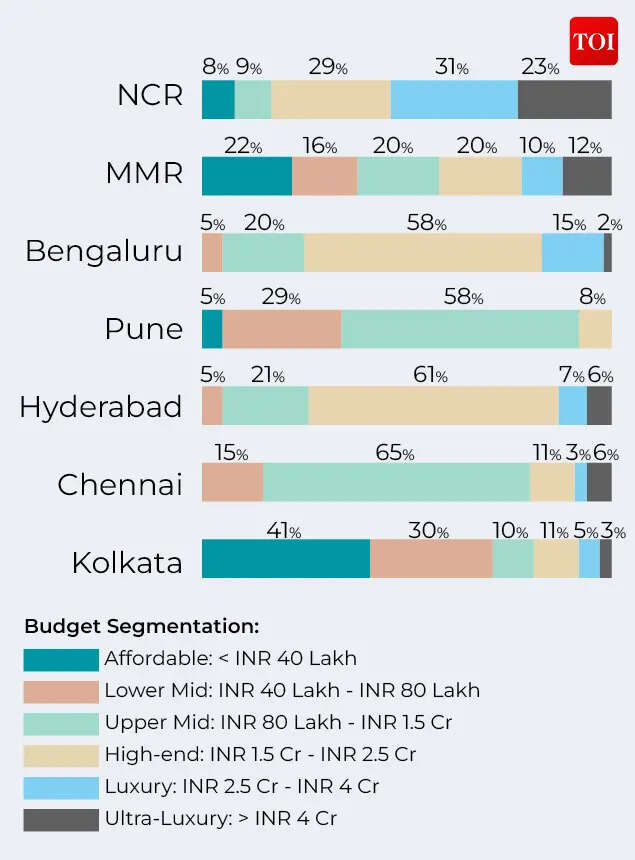

The primary driver is demand from affluent buyers.Developers increasingly view luxury and premium housing as more profitable because higher-income customers are better positioned to absorb price increases. As a result, the supply of affordable homes continues to shrink.The consequences are visible across the market.India currently faces a shortage of approximately 10 million affordable homes, according to Knight Frank projections. The deficit could triple by 2030 if current trends persist.Analysts say this mismatch between supply and demand is one of the biggest reasons why housing affordability remains under pressure despite a growing economy.

Cost of buying your ashiana

Whether you are looking to buy or rent a home, the biggest factor you need to consider is the cost. In case of rent, it’s not just about monthly rent, but also an annual rise in the rental cost, and in case you decide to switch houses then the costs associated with shifting homes.Most home buyers focus only on the EMI. But, the total cost of ownership includes stamp duty and registration, brokerage, interiors, furnishing, society maintenance, property tax, insurance and periodic repairs.

There is also the opportunity cost of the down payment. “If Rs 20 lakh is locked into a house instead of being invested elsewhere, that foregone return must be factored in. Over time, maintenance and renovation costs can meaningfully add to the effective annual expense, often making the real cost of ownership higher than initially assumed,” says Adhil Shetty.Another factor to keep in mind is the city you are looking to buy or rent a home in. Rohit Shah, financial planner points out: In high-growth, high-inflation markets like India, renting is often more economical. “Buying makes sense only when the EMI-to-rent gap is narrow—difficult in cities like Mumbai, where a Rs 2.4 crore 2BHK commands just Rs 55,000–85,000 monthly rent. That said, a first home bought for living—not investing—shouldn’t be a purely quantitative decision,” he says.Then there are interest rates that play a key role in your loan repayment. Any hike in interest rates over a 20 year loan period can increase your EMIs or lengthen your loan tenure. On the other hand, a rate reduction would work to your advantage. But when accounting for costs, it is prudent to keep in mind a rate hike scenario.Adhil Shetty, CEO of Bankbazaar.com says that interest rates directly affect affordability and the break-even timeline. For example, on a Rs 40 lakh home loan with a 20-year tenure, the EMI rises from about Rs 34,713 at 8.5% to about Rs 35,989 at 9%.

That translates into an additional outgo of roughly Rs 1,276 per month and about Rs 3.06 lakh in extra interest over the loan tenure.“Higher rates also extend the period required for ownership to outperform renting. On the other hand, sustained property price appreciation strengthens the case for buying,” he tells TOI.“However, price growth in many urban markets has historically been moderate compared to equities. Buyers should stress-test their decision against scenarios where rates remain elevated and property appreciation is modest, rather than assuming optimistic outcomes,” he adds.Yet another cost that people tend to overlook is how illiquid real estate is. “Real estate cannot be partially liquidated when cash is needed, and selling under pressure often means accepting a steep discount,” he tells TOI.

Economics of buying versus renting:

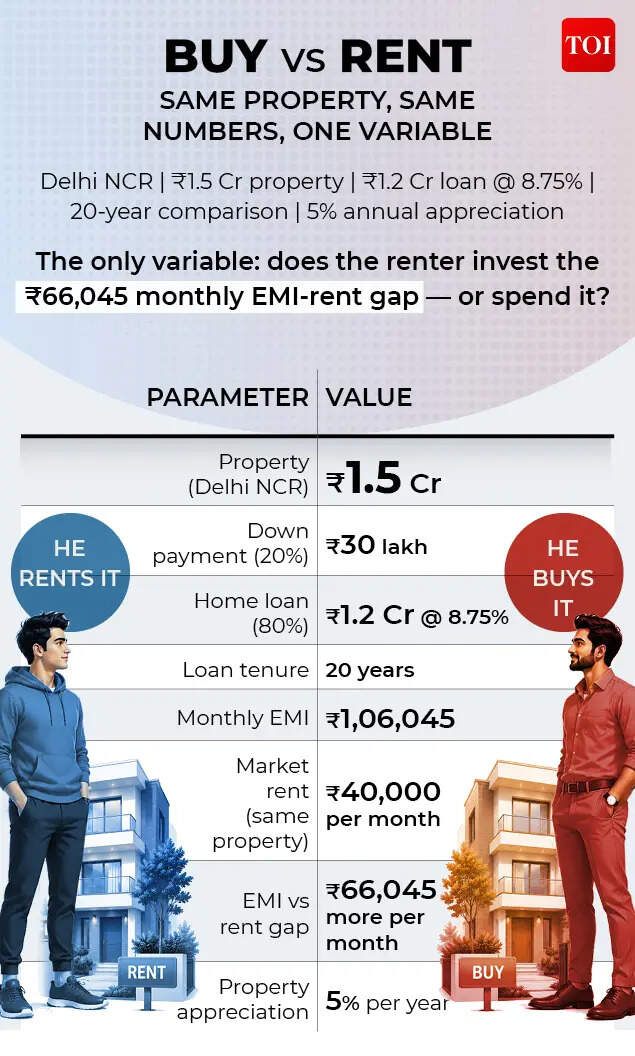

The economics of buying versus renting a home work differently depending on where you put your money. BankBazaar explains this with an example:You are looking at two people: a buyer and a renter of a Rs 1.5 crore property in Delhi-NCR. The 20-year loan of Rs 1.2 crore is assumed at an interest rate of 8.75%. An annual appreciation of 5% is assumed both in the property prices and rental rate.

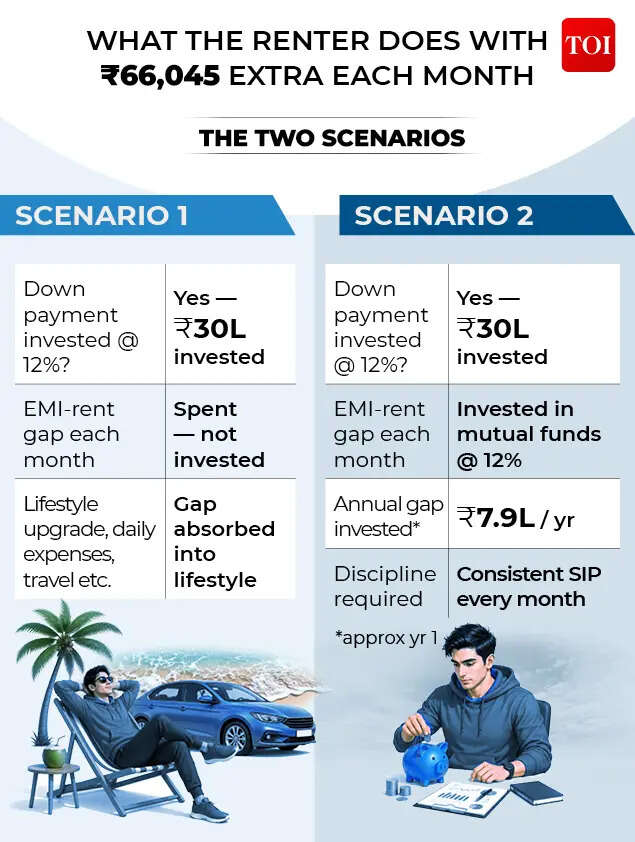

What is the biggest variable in returns? What the renter chooses to do with the difference between the EMI and rent payout.In the first scenario, the renter spends money on lifestyle upgrades. In the second scenario, the renter invests the gap in mutual funds that return around 12%.

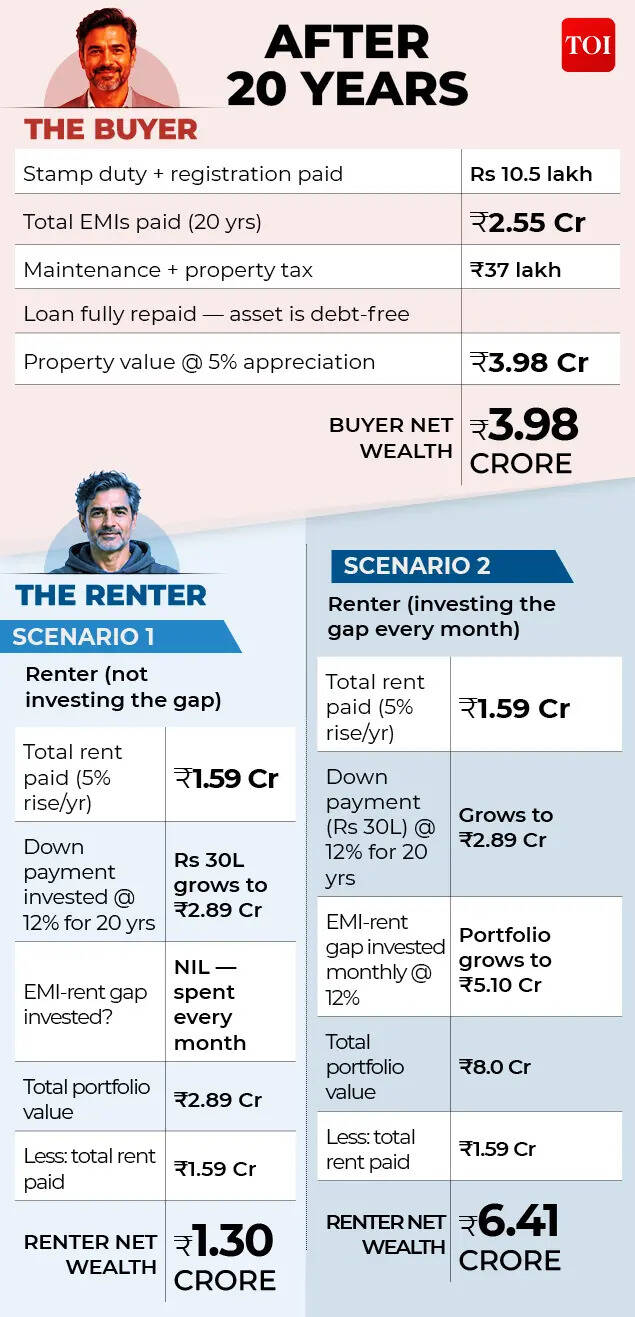

After 20 years, the buyer’s net worth is at an estimated Rs 3.98 crore after taking into account the EMIs, stamp duty and other associated costs such as maintenance and property tax.The renter on the other hand sees two very different scenarios playing out. If the renter has not invested the gap, then the net wealth is just Rs 1.30 crore. On the other hand, if the gap has been invested in a disciplined way, then the net wealth of the renter would be around Rs 6.41 crore.

To put it simply, in scenario one, the buyer emerges as winner with a margin of Rs 2.68 crore wealth, and in the second scenario, the renter wins with an additional net worth of Rs 2.43 crore.The fundamental takeaway in the above example is this: if the renter chooses to invest the gap between the rent and the EMI, then he is better off financially after 20 years. If however, the renter spends the gap on lifestyle choices, then the buyer emerges as a winner.It is important to note that the above example is broadly representative of a particular case. These figures will change depending on your financial situation and needs. Hence, the lesson from the above example is clear: doing your math before deciding on buying a home is absolutely essential.

How do real estate returns compare to other asset classes?

It’s not just about the cost of buying a house, if it is about treating it as an investment, then one wise way to do this is to compare it with other asset classes. The questions you need to ask yourself are: how do equities, mutual funds, fixed deposits, gold etc. compare to real estate in terms of returns, risks, and liquidity.According to Rohit Shah, the numbers are telling: Over the past decade, residential real estate has delivered 7–10% annually (capital appreciation plus rental yield of 3–5%), while equity mutual funds have returned 12–15%. RBI’s All-India House Price Index rose just 3.13% in FY25, which is barely above inflation. “A Rs 1 crore investment in equity mutual funds 15 years ago would have grown to roughly Rs 5.5 crore; the same in residential property would be approximately Rs 3.2 crore—a gap of Rs 2.3 crore, driven entirely by the power of compounding at even a 4% return differential,” Rohit Shah says.Equities and mutual funds offer liquidity, transparency and lower transaction costs. They can be bought and sold easily and allow diversification across sectors and geographies. Real estate, by contrast, is illiquid and concentrated. However, as Adhil Shetty points out, real estate offers leverage, tangible ownership and emotional security. Historically, long-term equity returns have tended to outpace residential property price growth in many cities, but real estate provides stability and utility value.“A primary residence should first serve housing needs. Viewing it purely as an investment can distort decision-making,” he tells TOI.Vivek Iyer, Partner and Financial Services Risk Advisory Services Leader, Grant Thornton Bharat offers a different perspective: From a financial planning standpoint, investing in real estate makes more sense than renting, as real estate serves as an effective inflation hedge with capital appreciation being more than the inflation rate. Comparing different asset classes from a risk and return standpoint is not fair, as every asset class meets a specific risk and return objective.

When does buying a home make sense?

According to Adhil Shetty, typically buying makes financial sense if you plan to stay in the property for several years, often seven years or longer. “Real estate involves high upfront costs such as stamp duty and registration, which can account for roughly 6% to 8% of the property’s value in many Indian cities. If you sell too early, these costs can significantly reduce returns,” he explains.Over a longer holding period, property appreciation, home-loan tax benefits for eligible borrowers and more predictable housing costs can tilt the equation in favour of ownership. “In the short term, renting is often cheaper. Over a longer tenure, the economics can shift, provided the purchase price is reasonable and borrowing costs remain manageable,” he adds.The bottom line is: your decision to buy or rent a home should be governed by multiple factors such as willingness to stay in a place for a lengthy period of time, rentals in the city, upfront buying costs such as stamp duties, registration, property taxes, risks and returns related to other asset classes. Real estate acts as a good investment option – what you need to know is whether you can afford it.But as we all know, owning a home is not just a financial decision, it is emotional, and that’s an aspect that cannot be ignored.