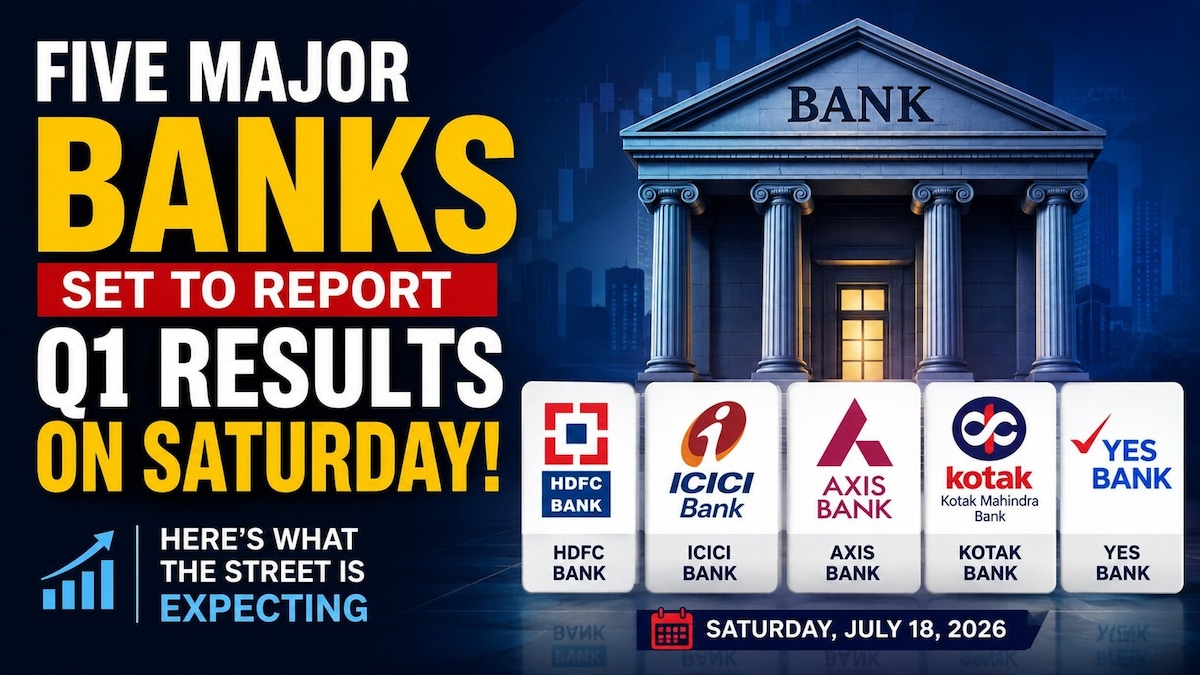

CNBC-TV18 has polled a panel of analysts ahead of the big bank results. Here’s a round up of what the Street is expecting this weekend from all these lenders:

Axis Bank

A CNBC-TV18 poll of analysts expect Axis Bank’s net interest income (NII) to come in at ₹14,870 crore, an increase of 10% from the previous year and 3% from the previous quarter.

The pre-provision operating profit (PPOP) is likely to decline 1% on an annual basis but gain 14% from the previous quarter to ₹11,379 crore in the June quarter.

Analysts expect the profit after tax (PAT) to increase by 18% to ₹6,877 crore from the previous year, but decline 3% from the previous quarter.

- NIM: The street broadly expects the net interest margin to be stable-to-marginally-lower, with the consolidated reading indicating roughly 0-10 basis points (bps) sequential pressure. Sticky deposit costs and stronger growth in relatively lower yielding corporate loans could be the main drags.

- Asset quality: Analysts expect Axis Bank’s asset quality to remain stable, although slippages may increase seasonally compared to the previous quarter. Credit costs are expected to stay contained, with some analysts expecting sequentially lower provisions. Stress in unsecured loans and credit cards is expected to continue easing.

- Other operating trends: The lender’s fee income is expected to remain healthy, operating expense growth should stay below business growth and lower bond yields could support treasury income.

HDFC Bank

The bank’s NII can rise 9% from the previous year and 4% from the previous quarter to ₹34,353 crore, as per the analysts poll.

Its Pre-Provisioning Operating Profit is expected at ₹28,605 crore, down 20% from the year-ago period but up 3% sequentially.

The bank’s PAT can rise marginally from the prior quarter (1%) to ₹19,332 crore and 6% from the previous year, as per analysts.

- NIM: The expectations range from stable to a marginal decline of around 5 bps sequentially. The gradual rundown of high-cost borrowings is supportive, but stronger growth in lower-yielding corporate loans and sticky deposits may limit near-term expansion.

- Asset quality: The street expects HDFC Bank’s asset quality to remain best-in-class. The previous quarter’s gross non-performing assets (GNPA) and net NPA levels were 1.15% and 0.38%, respectively. Slippages may rise seasonally, while provisions are expected to remain broadly stable.

- Other operating trends: The fee income growth could be softer than loan growth because of seasonality, while operating expenses should grow slower than the balance sheet, as per analysts.

ICICI Bank

NII: The lender’s NII or core income is set to rise 9% from the previous year and 3% from the previous quarter to ₹23,689 crore, as per street estimates.

Analysts see its PPOP coming in at ₹19,278 crore, up 3% from the previous year and 6% sequentially.

The bank’s PAT could increase 7% from the year-ago period to ₹13,616 crore in the June quarter. That number would be a 1% decline sequentially.

- NIM: Street expectations are stable to marginally lower quarter-on-quarter, broadly implying 0 to 5 bps pressure. The NIM had largely bottomed near 4.3% with medium-term FY27 estimate around 4.4%. A healthy business-banking and personal loan mix should offer support.

- Asset Quality: The street expects asset quality to remain among the strongest in the sector. The bank carries a provisioning coverage ratio (PCR) of around 76% and contingency provisions of approximately ₹13,100 crore, or 0.9% of loans. Its credit costs are expected to remain contained around 40 to 45 bps, although seasonal slippages and provisions may rise sequentially.

- Other operating trends: Recoveries, disciplined underwriting and strong portfolio monitoring should keep incremental stress under control. The lender’s operating expenses are expected to grow slower than business.

Kotak Mahindra Bank

The lender’s NII is expected to come in at ₹8,058 crore, up 11% from the previous year and 2% from the previous quarter.

The Street expects PPOP of ₹5,844 crore, the same as the previous quarter, but up 5% from the year-ago period.

Its PAT can rise 19% from last year to ₹3,910 crore. However, this would be 3% lower sequentially.

- NIM: Kotak Mahindra Bank is expected to face the sharpest NIM moderation among the large private banks. Some analysts expect a 14 bps sequential decline to approximately 4.53%, while others see stable-to-lower margins. The practical consensus is around 10 to 14 bps of sequential compression.

- Asset Quality: Analysts believe that the lender’s asset quality should remain broadly stable, with declining stress in microfinance and credit cards. However, credit costs and slippages may rise marginally on seasonal factors, and provisions are expected to higher sequentially in some estimates.

- Other operating trends: The street sees management commentary on restoring liability growth to be the main focus areas for Axis Bank.

Yes Bank

Yes Bank’s NII can increase 17% from the previous year to ₹2,772 crore. This would be up 5% sequentially as well.

Analysts expect its PPOP to increase 23% from the previous year and 3% from the prior quarter to ₹1,666 crore.

Its PAT can grow 37% to ₹1,100 crore from the year-ago period. This too will imply a sequential growth of 3%.

- NIM: The fourth quarter NIM was 2.7% and for the June quarter, the street expects it to be between 2.7% to 2.8%, supported by the continued rundown of low-yielding rural infrastructure development fund (RIDF) investments. However, the sharp fall in CASA and rise in the credit deposit ratio may restrict the pace of improvement.

- Funding position tightened: The calculated credit-deposit ratio increased sharply to 90.5% from 85.7% in the fourth quarter, reflecting faster loan growth and sequential deposit contraction. Deposit mobilization and CASA restoration will therefore by critical management commentary.

- Asset quality: The lender’s asset quality is expected to remain broadly stable, with the fourth quarter GNPA and NNPA coming in at 1.3% and 0.2%, respectively. The retail stress had been improving across secured and unsecured portfolios, while personal loan slippages moderated and credit card slippages remained stable.

- Key asset quality monitorable: Analysts said the bank’s retail slippages had improved to around 2.9% but remained elevated relative to its peers. Lower security receipt recoveries in FY27 could also lead to some normalization in reported credit costs despite stable underlying stress.

Shares of HDFC Bank are down 18% so far this year, while those of ICICI Bank, Axis Bank, Kotak Mahindra Bank and Yes Bank are up 6%, up 3%, down 15%, and up 10% respectively this year so far.