The brokerage now has a “buy” recommendation compared to its earlier rating of “neutral” on ONGC, along with a price target of ₹288 per share, from ₹265 earlier, which indicates an upside of 22% from its previous closing price.

According to Motilal Oswal, its upgrade is premised upon a combination of inexpensive valuations, a decent pick-up in volumes and on ONGC being a beneficiary of a multi-year government focus to turn around the sector.

While a peace MoU has been reached in West Asia, as per forecasts by the US EIA and Motilal Oswal’s view, the Organisation of Co-operation and Development (OECD) commercial inventories of crude oil and liquid products are unlikely to normalise for the calendar year 2026 and the first half of the calendar year 2027, according to the brokerage note.

This is likely to keep crude prices elevated, the brokerage said, adding that it has raised its brent price assumptions to $84.2 and $75 per barrel for FY27 and FY28 from the previous $75 and $65 per barrel, respectively.

Upstream back in favour for capital allocation

Globally, capital allocation is shifting towards upstream oil and gas after a decade of underinvestment amid declining oil and gas production and elevated crude prices over several years, as the recent West Asia crisis has brought to the fore the for countries to refill depleted inventories and expand strategic crude reserves, according to the brokerage.

Domestically, for both ONGC and Oil India, there has been an increased focus on finding new reserves and monetizing existing discoveries on a fast-track basis. Exploration and development efforts in overseas assets have also received a renewed lease on life and can unlock value due to elevated crude prices, it added.

Energy security could be a decade-long theme

Motilal Oswal believes energy security as a theme will remain a key focus for many years due to:

- India’s crude oil imports at 90% of total demand are unsustainably high

- India has under-invested in the upstream sector over the past decade, but the government now aims for domestic companies to take the lead with new initiatives such as Samudra Manthan.

ONGC’s Volume Growth Prospects

Motilal Oswal said it is modeling only a 2.6% volume compound annual growth rate (CAGR) for ONGC, aided by the start of DUDP, KG-98/2 and Samudra Manthan.

It said it is building in 40% dividend payout in FY27, which implies a 6% dividend yield at the current market price.

It said ONGC’s gas price realisation will continue to witness an uptick as 7%-8% of volumes every year qualify for higher new-well gas prices.

Standalone EBITDA estimates up

- The brokerage has increased its estimates for standalone profit after tax (PAT) growth to over 16% and 22% in FY27 and FY28.

- It has also raised its Brent assumption by $10 per barrel for FY28.

- Brent to average $80 per barrel in the second half of the FY27, Motilal Oswal added.

The brokerage believes that the timely start-up/ramp-up of the DUDP and KG-98/2 could boost ONGC’s earnings, given the strong price realization outlook.

Key Risks For ONGC

The brokerage listed the following key risks for the stock:

- Lower-than-expected crude oil and domestic gas realisations arising from a weaker commodity price environment.

- Delays in ramp-up or underperformance of key growth projects such as DUDP, KG-98/2, DSF blocks and Mumbai High.

- Adverse regulatory or fiscal changes, including higher government levies or changes in gas pricing mechanisms.

Of the 31 analysts who have coverage on the stock, 22 have a “buy” rating, five have a “hold” rating and four have a “sell” rating.

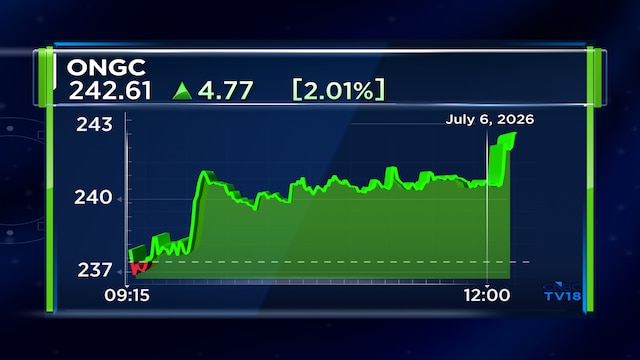

Shares of ONGC are trading 1.8% higher on Monday at ₹242.08. The stock is down 8.5% in the last one month and has therefore trimmed its year-to-date gains down to just 1.7%.

Also Read: These defence stocks are likely beneficiaries of the ₹52,000 crore procurement plan by DAC